Historic co-op buildings like the Dakota (lower left) and the San Remo (center, with twin towers) have retained their place within the top tier of Manhattan luxury real estate, while many newer condo buildings have come and gone. (Source: sbraia/Getty Images)

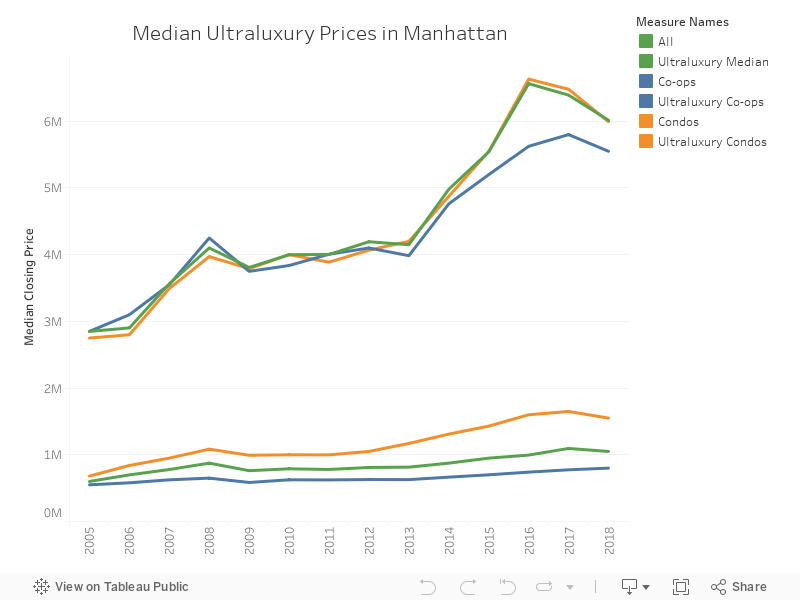

In Manhattan’s ultraluxury real estate market, price have doubled since 2005. This is the pinnacle of the Manhattan market, representing the top 10 percent of prices based on all sale closings in a given year — more pricey even than the traditional luxury market, which StreetEasy defines as the top 20 percent of closing prices.

From 2005 to 2017, the ultraluxury market saw its entry threshold rise from $1.9 million to $4.2 million. With median price growth averaging 8 percent per year, much faster than the 5 percent average annual growth rate of all Manhattan real estate over this period, these years represent a boom in ultraluxury housing, one fueled in part by wealthy foreigners who looked to New York real estate as a safe investment.

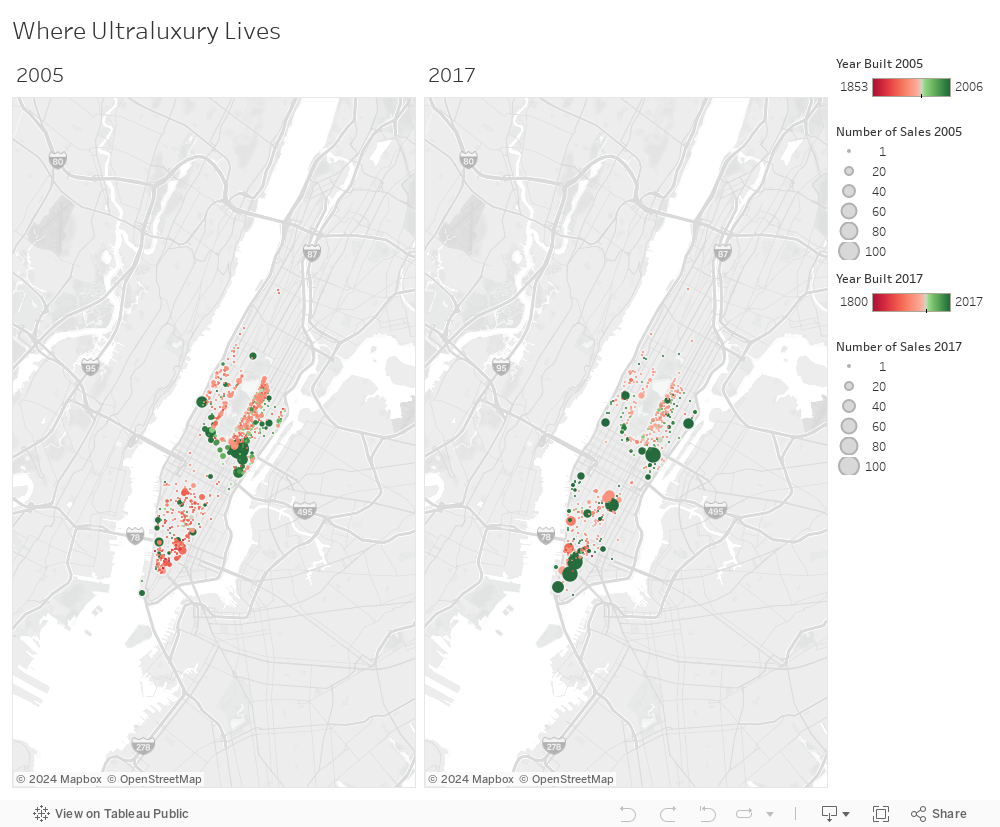

Significant changes in the ultra luxury market have accompanied this growth. Today’s top tier is more diverse in age and location than in 2005, as developers move downtown for more space, and as newer buildings take up a greater share of all sales. Notably, though, there remains a key place for older buildings in the ultraluxury tier.

Historic Buildings Retain Luxury Status Better Than New Condos

New developments — those built no more than two years ago — typically make up the largest portion of the ultraluxury market. However, our research finds that newer units, even some the most expensive on the market when built, tend to lose their place in the ultraluxury tier over time, as even newer, larger, more amenity-rich buildings come on the market to compete with them.

Of 23 new development buildings that occupied the ultraluxury market in 2005, only four, or 17 percent, remained in the same top tier in 2017. While the other buildings may have appreciated in value significantly, they did not sell within the highest segment of the market.

However, wealthy New York buyers have long looked favorably at historic buildings — those that the NYC Landmarks Preservation Commission has deemed to have cultural or historic value — such as the Dakota and the San Remo. Our analysis shows that over many repeat sales, these historic apartments have managed to retain their place in the ultraluxury tier despite an onslaught of high-end competition. In fact, 49 percent of the buildings that sold within the ultraluxury tier in 2005 and remained in 2017 were historic buildings. This suggests that historic buildings — the majority of which are co-ops — are more likely to retain their place within the ultraluxury tier than any particular new-development condo.

Overall, the share of co-ops and condos within the ultraluxury sphere has not changed greatly, rising from 25 percent and 71 percent, respectively, in 2005, to 18 percent and 77 percent, respectively, in 2017. New condo buildings simply fall out of the top tier as they age and are replaced with even newer, competing condos — many of which are being built in neighborhoods that only recently became appealing to luxury buyers.

Today’s Ultraluxury Market Is More Diverse in Age and Location

In 2005, new ultraluxury developments were concentrated in the Upper East Side, Upper West Side and Midtown West, especially along the southern border of Central Park and Park and Fifth Avenues. Since then, the ultraluxury market has spread out across the city’s various neighborhoods.

New developments accounted for 7.7 percent of ultraluxury buildings in 2017, compared to 3.1 percent in 2005, and the growth has been concentrated in Lower Manhattan, especially Tribeca, West Village, Nolita, and SoHo.

Boom in Ultraluxury Construction Led to Present Glut

The boom in ultraluxury real estate in Manhattan has been fueled in part by an expansion of international buying power. Since the recovery from the financial crisis, the world’s ultrarich population — those with net assets above $50 million— has grown by 18 percent, to 130,000 individuals in 2017.

Developers aim to capture demand from this expanding group by building the newest, tallest and most architecturally innovative residential buildings in New York City. Meanwhile, wealthy individuals — whether they be Russian oligarchs, Chinese property magnates, or American hedge-fund managers — continue to purchase these homes as investments and status symbols. In 2017, foreign buyers spent $153 billion on residential property in the United States, a 49 percent increase from the prior year.

This boom in ultraluxury development shows few signs of slowing down, as new buildings reach supertall status almost weekly. However, these buildings are rising at a faster pace than the world’s population of multimillionaires is increasing. Since 2015, price growth in the top tier has slowed significantly to an average annual rate of 2 percent, compared to 7 percent before, and units have piled up on the market. As of the third quarter of 2018, almost 20 percent of all StreetEasy sales listings consist of apartments in the ultraluxury tier, with prices starting at $4 million.

In a city with an affordable housing crisis, developers are building more ultraluxury towers than there is demand for them. It remains to be seen how sustainable this trend will be.

How We Did It

We define the ultraluxury market as the sales closings priced at the top 10 percent of all sales in a given year. StreetEasy generally defines the luxury market as the top 20 percent of sales, so ultraluxury is a distinction for the top 10 percent. We categorize building as being in the ultraluxury market if it has had at least one unit for sale priced in the top 10 percent. Data on sales prices and number of closings between 2005 to 2017 reflect all sales in New York City, as reported to the NYC Department of Finance. We looked at 2005 because it is the first full year for which the City has closings data for co-ops. Figures on price per square foot refer only to condo units listed for sale on StreetEasy. We define new development buildings as any building constructed within the past two years from the year of reference, and all new developments in our data are condo units. We define historic buildings using building data from the NYC Department of City Planning, as specified by the NYC Landmarks Preservation Commission. Historic buildings require approval from the LPC for any alterations or demolitions.

—

Hey, why not like StreetEasy on Facebook and follow @streeteasy on Instagram?