(Photo by Hero Images/Getty Images)

So, you got into the college of your dreams. Congratulations! But now you need to figure out how you’re going to pay for it. And as well all know, college doesn’t come cheap. After factoring in scholarships, grants and other forms of financial aid, it’s still more than likely that you’ll turn up short. That’s where student loans come in.

You should think over student loans very carefully before deciding to apply for or accept them. According to StudentLoanHero, Americans owe more than $1.48 trillion in student loan debt, and the average student loan debt for Class of 2017 graduates was $39,400. It’s easy to let them pile up, and they can plague you long, long into your adulthood. (Just check out these horror stories if you don’t believe us.)

So here’s our advice on how to save on college costs, apply for loans, and make budgeting decisions.

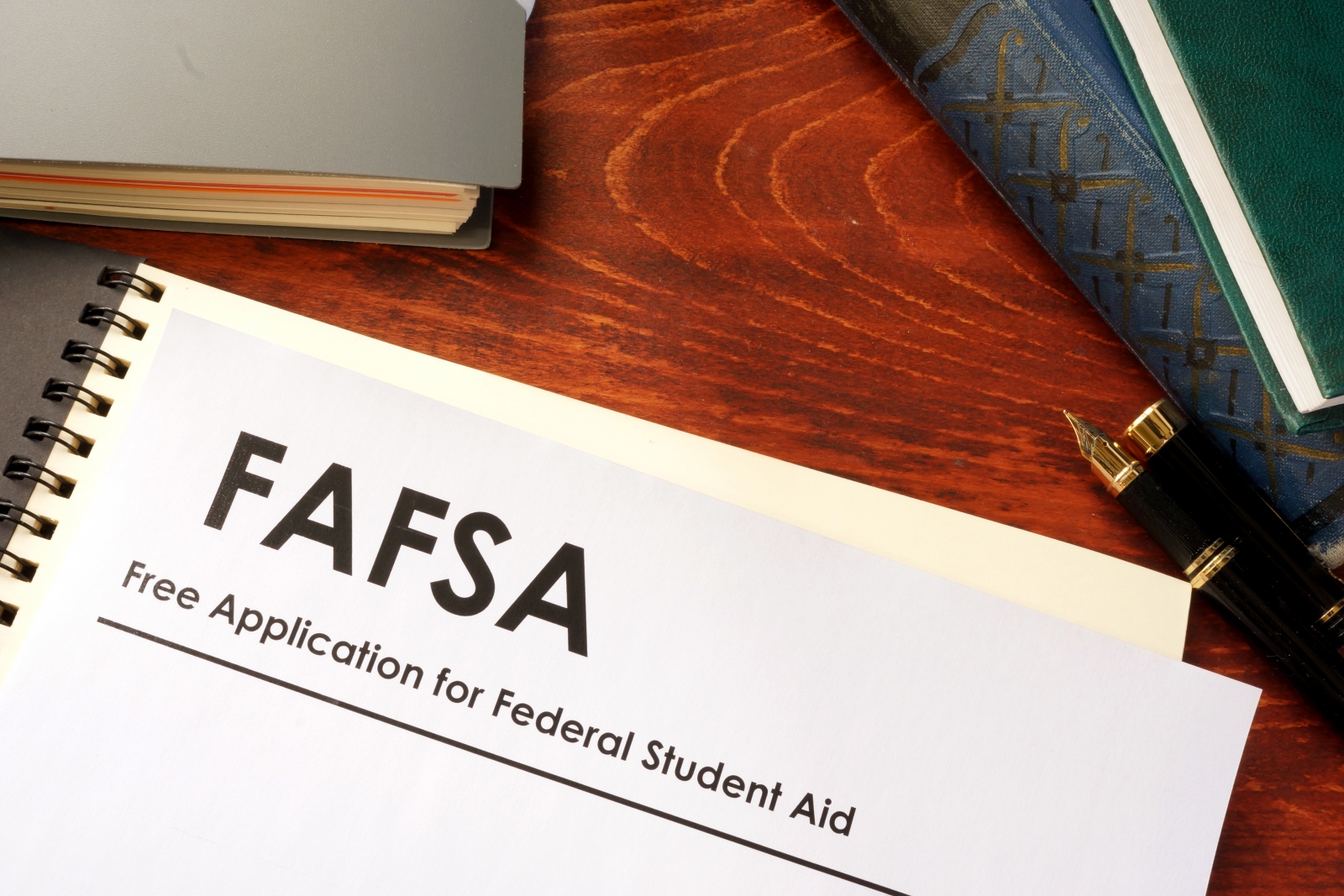

Apply for financial aid and scholarships before considering loans

(Photo by designer491/Getty Images)

While many might think they don’t qualify for financial aid, it’s always worth applying, especially because it’s free. Students should be sure to fill out the FAFSA (Free Application for Federal Student Aid) every single year. This can help them qualify for grants from their schools, as well as from the federal government, such as Pell grants and Supplemental Educational Opportunity Grants.

Those who don’t qualify for grants, which are need-based, might still qualify for scholarships, which are merit-based. Students who don’t have much luck with scholarships from their colleges aren’t out of luck yet. There are plenty of privately funded scholarships out there. Scholarships, like grants, are great because they’re basically free money — they don’t have to be paid back.

Sites like Niche and Scholarships.com are great for finding available scholarships. It’s best for applicants to cast their net wide and apply for anything they think they might be eligible for; these scholarships are typically pretty competitive, so it’s best to apply to a lot.

How to cut down on costs

One way to cut down on the amount of loans taken out is to work during college. Students who are from New York and are staying for college have probably have had a job here at some point; they should hold onto it and see if they can work part-time during school.

Those who are going away for college should look into their school’s work-study program. These programs allow students to work right on campus, so they won’t have to travel far. They’ll make new friends and interact with more of the campus community, too.

Some students think that working during college is too difficult, along with juggling classes, social time, and extracurriculars. But having a job while in school will teach students valuable skills like time management, helping them value the time they do have off. Plus, that paycheck doesn’t hurt, whether they’re using it to pay for rent, books, or part of tuition.

It’s important to remember: any money that students can make now and actively put toward their education is much more valuable than money they’ll make later to pay off loans with massive interest rates.

Applying for loans

(Photo by westend61/Getty Images)

But if after exhausting your “free money” and work options, you still need to take out a loan, you have a few options. Federal loans mean that you owe the government money, while private loans mean you owe a bank or private lender money. Typically, federal loans have lower interest rates than private loans, so you should always start there before you consider private loans.

Federal grants also are divided into two categories: subsidized and unsubsidized. Subsidized loans won’t start accruing interest until six months after you graduate, while unsubsidized loans start accruing interest the day you take them out. It’s always a better idea to take the subsidized loan if you qualify for it, as they’re typically reserved for lower-income students.

Students who do decide to apply for a private loan should make sure to read all the information on the lender before they apply. Just because the starting interest rate is low doesn’t mean it’ll stay that way. Reading testimonials and reviews and discussing with a trusted adult — who will probably have to cosign the loan anyway — can also be a big help in the decision. Check out the top six private student loaners here, according to NerdWallet.

Using student loans for living expenses, e.g., rent

(Photo by zimmytws/Getty Images)

If a student does take out a student loan, it will typically go directly to their school to cover the cost of tuition, fees, etc. However, if the amount of the loan exceeds their amount of college costs, then there will be money leftover, called a student loan refund. This money will be disbursed to the student via check, cash, or credit to their bank account. The student can then use the money for whatever they want, such as books, rent, living expenses, groceries, etc. They can also return it to the lender to cut back on the amount they will need to pay back later.

So can students use student loans to pay for their rent? Yes. But should they? Probably not.

Most experts and writers on the topic say that using a student loan to cover rent or any extra costs is not prudent. Any money that students take out now is money that they’ll have to pay back later, undoubtedly becoming a much greater amount while it accrues interest.

And even though New York rent can be expensive, it’s better to know that you are paying for it as you go, and that those monthly payments won’t come back to haunt you for years.

To learn more about student loans, visit the official website for Federal Student Aid.

—

Hey, why not like StreetEasy on Facebook and follow @streeteasy on Instagram?