Buying Your First Home in NYC

Buying a home in NYC is complicated, but rewarding. If you're a first-time home buyer, or even a returning buyer who needs a refresher, this guide will provide you with tips and strategies for your home-buying journey.

A few of the topics covered in this guide include: how to find your dream home, how to find a buyer's agent, how to prepare for a co-op board interview (and what even is a co-op vs. a condo?), information about home inspections, home loans and mortgages, and much more! We hope these articles will help you make educated decisions and feel a little more confident as you begin this journey — whether you're a first-time home buyer or a real estate veteran. Happy home shopping!Key takeaways:

- Buying a home in NYC is complex and competitive, but preparation and understanding the process can make it manageable and rewarding.

- Deciding to rent or buy depends on factors like how long you plan to stay, your financial readiness, and your desire to build equity and customize your space.

- NYC buyers typically must choose between co-ops and condos, with co-ops usually cheaper but more restrictive, and condos offering greater flexibility at higher costs.

- Upfront costs are significant: buyers should budget for a substantial down payment, closing costs of roughly 4–6%, and ongoing costs like maintenance fees or common charges.

- Getting mortgage preapproval early and working with an experienced buyer’s agent can strengthen offers, improve negotiation power, and reduce stress throughout the process.

The New York City real estate market is like no other, characterized by high price points, unique complexity, and tough competition. Nevertheless, always up for a challenge, many New Yorkers still dream of owning a home in the five boroughs. The process can be intimidating — especially for first-time home buyers — but the rewards are immense.

In this guide, we break down everything you need to know about buying a home in NYC.

Should you rent or buy?

Buying a home in NYC is no small feat. Prices here are notoriously high — higher than other parts of the country, even when there’s a dip in the market. No wonder so many New Yorkers rent! But how do you decide between renting and buying?

If you’re considering buying, ask yourself these questions:

- Do you plan on staying put for a while? If not, it might make more sense to rent. “The benefit to renting is flexibility,” says Steven Gottlieb, a licensed real estate salesperson with Coldwell Banker Warburg. “If you experience a life-changing event, like job relocation or familial changes, it’s much easier to pick up and move. You don’t have a large real estate asset to worry about selling.”

- How are your finances? Renting also allows you to remain more financially fluid. There’s no down payment or closing costs to shell out, and from a maintenance standpoint, most repairs — plumbing, electric, etc. — are the landlord’s responsibility, not yours.

- Do you love a particular neighborhood? Try “test driving” a neighborhood by renting or spending a lot of time there before you make a longer-term commitment. Learn about your surroundings, figure out commute times, and get a vibe. If you’ve fallen in love with a neighborhood, buying is a great way to make it your forever home.

- Do you like to customize your space? If you own your home, you can hammer, drill, paint, and fully renovate it to your heart’s content. If you rent, your ability to customize your space is much more limited, and you’re putting money and labor into something you don’t own.

- Do you want to build wealth? “Buying a home in NYC is an investment, both in terms of building equity and in tax and mortgage deductions,” says Parisa Afkhami, a StreetEasy Expert and licensed real estate salesperson with Coldwell Banker Warburg.

How much does an NYC home really cost?

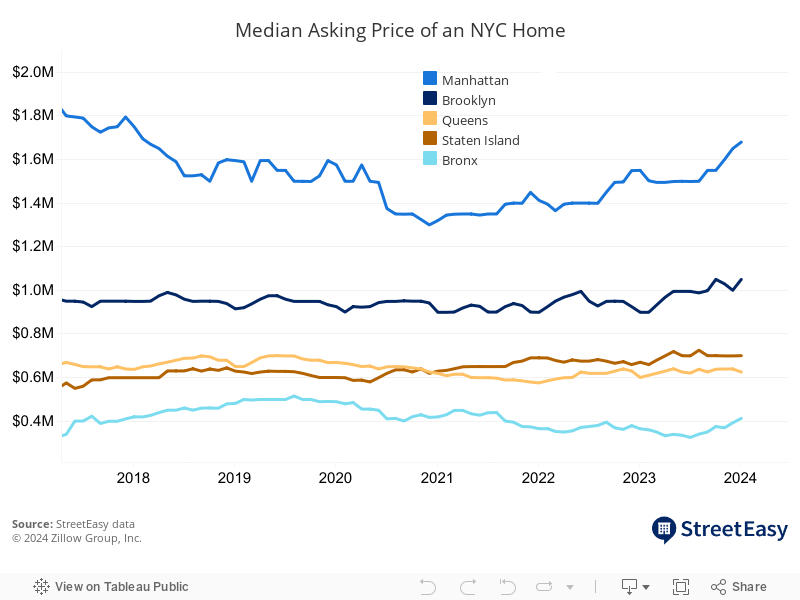

As in many cities, it depends on where you look, and the current state of the local housing market. In NYC, it also depends on what kind of home you’re buying: co-op, condo, townhouse, etc. (more on these in the next section). You can check the StreetEasy Data Dashboard for the latest median asking prices by borough or neighborhood, as well as other data such as inventory and days on market.

In 2025, the median asking price for a home in each borough was:

- NYC: $999,000

- Manhattan: $1,350,000

- Brooklyn: $1,100,000

- Queens: $700,000

- Bronx: $399,000

- Staten Island: $769,000

There’s no perfect time to buy, but it doesn’t hurt to keep tabs on the latest NYC housing market trends. Turn to the StreetEasy Data Dashboard for up-to-date median asking prices, inventory, days on market, and more.

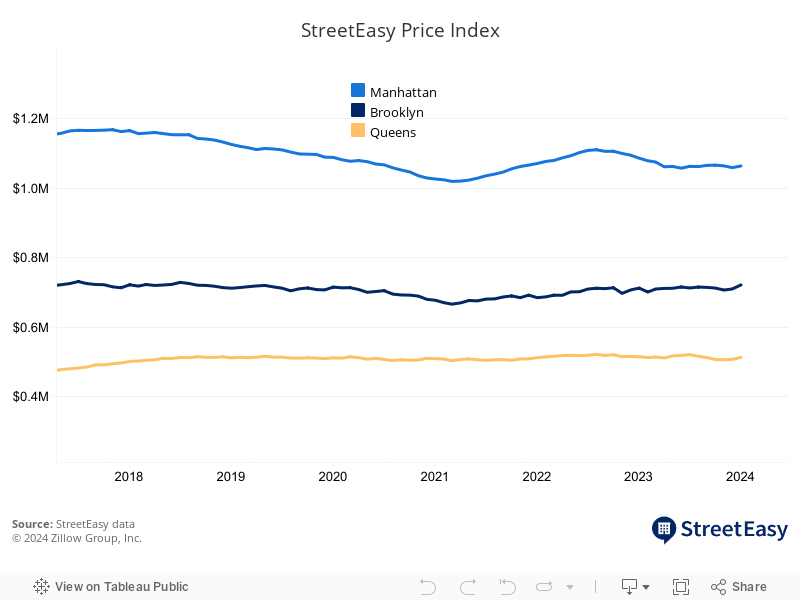

Additionally, the StreetEasy Price Index provides an accurate measure of home prices in NYC:

In addition to your monthly mortgage payment, you’ll pay standard costs like taxes and utilities. You’ll also be responsible for costs that aren’t common in other cities, like maintenance fees for co-ops or common charges for condos (more on these in the next section). Of course, this is after making a substantial down payment and paying closing costs.

Keep in mind that prices are almost always open to negotiation. “There’s no decision to make until you’ve negotiated something down,” says Mike Fabbri, StreetEasy Expert and licensed real estate salesperson with The Agency. “I encourage buyers to look 10% to 15% above their budget, with the expectation we can negotiate it down. Then we narrow in on two or three properties, and we make multiple offers. Whichever one we get the best deal on, we move forward with.”

Also know that condos tend to cost more than co-ops. But, while co-ops might be cheaper, you’ll have to undergo the highly involved process of being approved by the co-op board. There are also strict down payment minimums, sometimes higher than the typical 20%, and other rigid financial requirements — a big ask for many first-time buyers.

Co-op or condo?

You may be wondering about this distinction that seems unique to the New York City real estate market — and it is. One of the many quirks of buying a home in NYC is that you need to decide between purchasing a co-op or a condo. There are also “condop” buildings, which have elements of both; townhouses, meaning single-family homes that share at least one wall with another residence; and traditional standalone homes in some areas.

What is a co-op?

A co-op is a type of property in which buyers are actually purchasing shares of a corporation, and that corporation or “co-op” owns the building. Typically, the size of your unit corresponds with the number of shares you own. Prospective buyers have to be approved by the co-op board (with the exception of sponsor units) — a process that usually involves an interview, references, and meeting strict financial requirements. Co-op owners are also required to pay monthly maintenance fees, covering the building’s taxes and operating costs, and abide by the rules set by the co-op board, which are usually more numerous and strict than those of condos.

The majority of residential buildings in NYC are co-ops, but when searching for homes on StreetEasy, you’ll notice a more even split between co-ops and condos.

What is a condo?

If you choose to buy a condo, you own the unit itself, and you jointly own the common areas of the building along with the other residents. Condos tend to be found in newer buildings with more amenities, are usually more expensive than co-ops, and have higher closing costs (more on these in the next section). Instead of maintenance fees, condo owners pay common charges, which cover similar things like building upkeep and operational expenses. Condo buildings have boards, but the approval process for buyers is much less intense than it is for co-ops. Condo owners are usually subject to fewer rules, with more flexibility on things like subletting and pied-à–terres.

Read our full explainer on co-ops vs. condos for more pros and cons of each, and how to decide which one is right for you.

Closing costs, taxes, and fees when buying an NYC home

In addition to the home’s list price, you’ll need to factor in closing costs, which are extra costs due at closing when finalizing the deal. They typically amount to 4-6% of the home’s purchase price, and are higher for condos than for co-ops.

Closing costs usually cover a real estate attorney, bank attorney, mortgage origination fee, appraisal fee, mortgage recording tax, title insurance, and more. If you purchase a home costing $1M or more, you’ll have to pay a mansion tax of 1-4%. And don’t forget the cost of renovations, if that’s also part of your buying journey.

“There are always unexpected fees, so it’s always worth asking upfront,” says Fabbri. “A good broker will find out everything for you before you even consider an offer.”

Is there a best, or cheapest, time to buy a home?

Timing the market is tricky, but no matter what’s happening, the right time to buy will always be whenever it’s right for you. If you’re financially prepared, and you need to move soon due to life changes — a new job, a growing family, etc. — it may be as good a time as any to start the process.

There are a few rules of thumb buyers can follow. The NYC market is highly seasonal, and typically, inventory peaks between April and June and then bubbles up again in October. Price cuts also rise in the spring and fall, especially after Memorial Day and Labor Day. You can observe these trends when looking at historical data using the StreetEasy Data Dashboard.

That said, bucking seasonal trends can be a great way to find opportunities. Buying in fall, for instance, can mean less competition and more discounts. Speaking of price cuts, when a listing has been on the market for a while — which tends to occur more during off-peak seasons — the seller may be more willing to negotiate on price.

“When you buck the herd mentality, there is an opportunity awaiting. Simple risk-reward economics at work,” says licensed real estate salesperson Karen Kostiw of Coldwell Banker Warburg.

Interested in buying a home in NYC? Get in touch with our complimentary StreetEasy Concierge to learn about the NYC buying market and more.

What’s a typical down payment on a home in NYC?

The standard down payment on an NYC home is in line with the rest of the country: 20%, leaving 80% to financing. Some co-ops have stricter requirements, such as only allowing 75% financing (a 25% down payment). Some condos will allow up to 90% financing, making homeownership a little more accessible to first-time home buyers.

But economic uncertainty has changed things. “Many co-ops have changed their financing policy,” says Steven Goldschmidt, Senior Vice President of Coldwell Banker Warburg. “They’re reducing the maximum allowable financing and requiring buyers to put up more equity. For example, some co-ops that allowed up to 80% financing have now reduced the maximum to 70%.”

Banks may also ask for a larger down payment. While many are still looking for a 20% down payment, other banks require more. Some will finance as much as 90% of a purchase price up to $3.5 million.

Regardless of requirements, the general wisdom is that the more money you can put down, the better. “Someone paying all cash or only financing 50% or less will have more leverage in negotiating with a serious seller,” says Fabbri.

Should you get preapproved for a mortgage before starting your search?

Whether you’re a first-time or repeat buyer, it’s essential to get preapproved for a mortgage when shopping for a home. Preapproval is a formal process in which a mortgage lender determines if you qualify for a mortgage of a certain value. Sellers strongly prefer a preapproved buyer, and it can give you an edge when a home has multiple offers. Note that preapproval is not the same as prequalification — the latter is less formal and doesn’t hold as much weight.

“Being preapproved will give you the upper hand over another buyer who isn’t,” says Alexander Boriskin, a licensed real estate salesperson with Douglas Elliman. “Sure, they can get preapproved at the request of the seller. But the person who comes in and shows that they already have their ducks in a row will be considered less of a risk, in most scenarios.”

Preapproval is also helpful for you, the buyer, because it gives you an idea of what you can afford based on the loan you qualify for.

Do you need a buyer’s agent?

When buying a home in NYC, using a buyer’s agent can make the process a lot less stressful. Why? Because they do most of the work for you. “A buyer’s agent will handle all the details and keep you aware of any concerns or pitfalls,” says Gerard Splendore, a licensed associate real estate broker with Coldwell Banker Warburg.

A buyer’s agent often has in-depth knowledge of the local real estate market, down to the neighborhood you’re pursuing. In addition to walking you through the buying process and attending showings with you, they can help you come up with a bid, negotiate with the seller, recommend a mortgage broker, connect you with a real estate attorney, and more.

If you want a buyer’s agent with the utmost localized knowledge of the NYC market, consider working with a StreetEasy Expert. They have verified experience helping buyers purchase homes in the neighborhood, building, or type of property you’re seeking. Reach out to the StreetEasy Concierge for buyers to be matched with the best Expert for your needs.

How to put a winning offer on an NYC home

Coming up with a winning bid is both an art and a science, and it’s another area where a buyer’s agent comes in handy. It’s up to you to offer what you’re comfortable with, but an agent can help you arrive at a strategic bid that will appeal to the seller and stand out from the competition.

And a winning offer is about more than just the dollar amount: it’s the whole package. Work with your agent to put together a buyer’s packet, including all the necessary financial, employment, and tax documentation.

Manhattan Homes Under $1.5M on StreetEasy Article continues below

Your offer was accepted! Now what?

Once your offer is submitted and accepted, it’s tempting to exhale and consider yourself a first-time home buyer. But don’t relax just yet! The next step is signing the contract, and there’s a deposit involved.

“When the final draft is approved by both sides, the buyer will sign the contract and return it with a contract deposit,” also known as earnest money, says Splendore. “This is typically 10% of the sale price, a ‘good faith deposit’ that goes toward the purchase price of the property.”

Brooklyn Homes Under $1M on StreetEasy Article continues below

What happens between signing and closing?

Once the contract is signed and the funds clear, you’re almost at closing. Co-ops, and some condos, require submission of a board package, which includes various financial, employment, and tax documents. Your mortgage lender needs to process all the necessary paperwork, too. All in all, the time between offer and closing is typically 30 to 45 days, but two months is a good estimate to be on the safe side. For more on what to expect during this period, and how long it takes, see our article on how long it takes to close on a home.

The time between signing and closing is all about waiting on the bank and the co-op or condo board. Generally, there’s an evaluation by the board, plus various inspections, appraisals, and walk-throughs. It can take a while — as in, months — and depends on if it’s a co-op or condo, how you’re financing the purchase, and other factors.

While the bank is working on the mortgage paperwork, buyers should avoid major purchases or accruing any unusual debt. “I advise buyers to keep all accounts current during this time,” says Splendore. “Don’t open any new accounts with credit card companies or stores, either.”

Queens Homes Under $1M on StreetEasy Article continues below

What to expect at closing

The short answer is: a lot of paperwork! Closing is usually a drawn-out process involving signing documents and exchanging large amounts of funds. The attorneys on each side of the transaction (buyer and seller) will keep everything moving.

It’s a long step, but it’s the final step. And in the end, you’re a homeowner — in New York City! Congratulations on making the center of the universe your forever home.

Ready to buy a home in NYC?

Start your search hereStreetEasy is an assumed name of Zillow, Inc. which has a real estate brokerage license in all 50 states and D.C. See real estate licenses. StreetEasy Concierge team members are real estate licensees, however they are not your agents or providing real estate brokerage services on your behalf. StreetEasy does not intend to interfere with any agency agreement you may have with a real estate professional or solicit your business if you are already under contract to purchase or sell property.