Data from April suggests that the NYC for-sale market may be picking up after its 2018 slump. (Getty Images)

The number of for-sale homes going into contract spiked in April, particularly in Manhattan, an indicator that the NYC sales market may be strengthening. Pending sales [i] in Manhattan increased 26.6% from last year, reaching their highest levels since the spring of 2015 — an encouraging sign for New Yorkers looking to sell their homes this year.

While more homes went into contract, fewer hit the market. There were 9.6% fewer homes listed for sale in Manhattan this April compared to last year, and total sales inventory available in the borough grew at the slowest pace in a year. In Brooklyn and Queens, inventory growth slowed significantly from the highs we saw in March. New inventory increased by 2.2% in Brooklyn and 13.4% in Queens in April, compared to an increase of 31.6% and 26.3%, respectively, in March.

Price growth remained weak across Manhattan, Brooklyn and Queens. The StreetEasy Manhattan Price Index [ii] fell to $1,105,595 — down 5.2% from last year and the largest drop since the financial crisis. Prices in Brooklyn were also down 0.4% from last April, dropping to $706,582. In Queens, prices continued to grow, but at the slowest pace since 2016 — up 2.4% to $516,739.

“While many sellers are still struggling to attract a buyer, April brought some good news to those who have feared a continued slide in the sales market,” says StreetEasy Senior Economist Grant Long. “Early signs tell us that some sellers are finally pricing their homes more realistically and finding buyers when they do so. Those still struggling to find the right buyer should take this as a sign to revisit their pricing expectations. Buyers are out there, but with most of the bargaining power in their hands, they’re going to continue to hold out for more reasonable prices.”

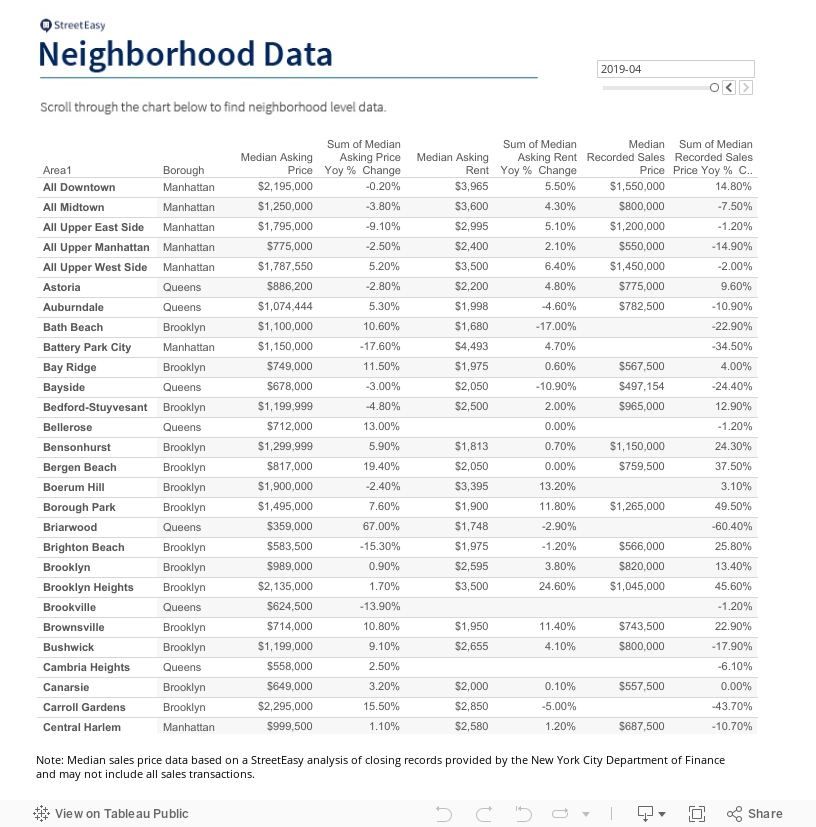

See below for additional sales and rental market trends across Manhattan, Brooklyn and Queens.

April 2019 Key Findings — Manhattan

- The most homes went into contract since 2015. The number of pending sales in Manhattan increased 26.6% from last year, up by more than 250. The number of homes entering contract in Upper Manhattan [iii] doubled year over year, from 66 to 132.

- Inventory growth slowed. While sales inventory growth remained in the double digits at 10.8%, it still moved at the slowest pace in 13 months. The volume of new inventory hitting the market shrank by 9.6% over last year.

- Prices continued to drop. The StreetEasy Manhattan Price Index fell 5.2% from last April — down by $60,096 to $1,105,595, the lowest level since May 2015.

- As sellers priced homes more strategically from the start, fewer made price cuts. The share of homes with a price cut fell slightly for the first time in 13 months. Some 14.1% of Manhattan homes saw a price decrease in April — down 0.6 percentage points from last year. The share of price cuts fell the most in the Upper West Side [iv] — down 2.1 percentage points to 14.2%.

- Luxury home inventory dropped slightly. The number of homes for sale priced within the top 20% of the market fell by 0.3%, the first year-over-year decrease in inventory since February 2018.

April 2019 Key Findings — Brooklyn

- Pending sales rose the most in the city. Of the boroughs analyzed, the number of homes entering contract grew the most in Brooklyn — up 30% from last April.

- The pace of inventory growth slowed. In April, 2% more homes were added to the market than the same time last year, pushing for-sale inventory in Brooklyn to a new high.

- Brooklyn prices stagnated overall, and dropped significantly in North Brooklyn. The StreetEasy Brooklyn Price Index fell just 0.4% since last year to $706,582. In North Brooklyn [v], the borough’s most expensive submarket, prices fell at the fastest pace since 2011 — dropping 2.0% to $1,120,548.

- The share of price cuts rose slightly. Boroughwide, 11.6% of homes for sale were discounted — up 1.5 percentage points from last year. All five submarkets in the borough had an increased share of price cuts, though North Brooklyn saw the most, with its share of discounts increasing by 1.8 percentage points to 11.7%.

- Homes spent more time on the market. Brooklyn homes for sale spent a median of 60 days on the market in April — up 11 days from last year. Homes in South Brooklyn [vi] came off the market three days faster than this time last year, to a median of 65 days on the market.

April 2019 Key Findings — Queens

- More homes entered contract than last year. Following a similar trend as the rest of the city, Queens saw 10% more pending sales than last April. In Northwest Queens [vii], 4.1% more homes entered contract over last year, but the submarket experienced a significant drop from the month prior, with 100 more pending sales in March than in April.

- Sales inventory growth slowed. While total inventory rose by 21.1% in the borough, it was the smallest increase since last summer. New inventory added to the Queens sales market in April was up by 13.4% year-over-year.

- Prices grew, but at the slowest rate in two years. The StreetEasy Queens Price Index reached $516,739 — up 2.4% from last year. Price growth in the borough showed signs of slowing from the higher rates seen since 2016, including the peak growth rate of 7.3% which occurred in June 2018.

- Price cuts rose slightly. The share of price cuts in Queens was the smallest out of the boroughs analyzed at 9.9%, up 1.3 percentage points from last year. Northwest Queens saw a decrease in the share of price cuts — down 2.6 percentage points to 12.4%

- Homes spent more time on the market. Homes in Queens spent a median of 57 days on the market — an increase of 9 days from last year, but the shortest period of the boroughs analyzed.

View the complete StreetEasy Market Reports for Manhattan, Brooklyn and Queens with additional neighborhood data and graphics. See definitions of StreetEasy’s metrics and monthly data from each report.

[i] StreetEasy defines pending sales as homes that are in contract. An offer has been made and accepted, and the closing is pending.

[ii] The StreetEasy Price Indices track changes in resale prices of condo, co-op, and townhouse units. Each index uses a repeat-sales method of comparing the sales prices of the same properties since January 1995 in Manhattan and January 2007 in Brooklyn and Queens. Given this methodology, each index accurately captures the change in home prices by controlling for the varying composition of homes sold in a given month. Levels of the StreetEasy Price Indices reflect average values of homes on the market. Data on the sale of homes is sourced from the New York City Department of Finance. Full methodology here.

[iii] The Upper Manhattan submarket includes Hamilton Heights, Washington Heights, Inwood, West Harlem, Central Harlem, East Harlem, Manhattanville and Marble Hill.

[iv] The Upper West Side submarket includes Lincoln Square, Upper West Side, Manhattan Valley and Morningside Heights.

[v] The North Brooklyn submarket includes Greenpoint and Williamsburg.

[vi] The South Brooklyn submarket includes Sunset Park, Bay Ridge, Dyker Heights, Bensonhurst, Bath Beach, Gravesend, Borough Park, Kensington, Coney Island, Brighton Beach, Ditmas Park, Seagate, Flatbush, Midwood, Sheepshead Bay, Manhattan Beach, East Flatbush, Canarsie, Flatlands, Marine Park, Bergen Beach, Old Mill Basin, Greenwood and Gerritsen Beach.

[vii] The Northwest Queens submarket includes Astoria, Long Island City, Sunnyside and Ditmars-Steinway.

—

Seeking your next place in New York? Whether you’re looking to rent or to buy, search NYC apartments on StreetEasy.