For New Yorkers considering buying a home, 2017 has been a tough year. A combination of rising mortgage rates and higher home prices in many parts of the city have decreased the affordability of purchasing a home. Moreover, a softening in the rental market throughout the city has made renting more attractive relative to buying, causing some potential homeowners to postpone their purchase. Given these circumstances, the latest StreetEasy Tipping Point analysis shows buyers should be prepared to spend a longer time in their home than in the past for their home purchase to pay off.

NYC’s Tipping Point is 5.6 Years

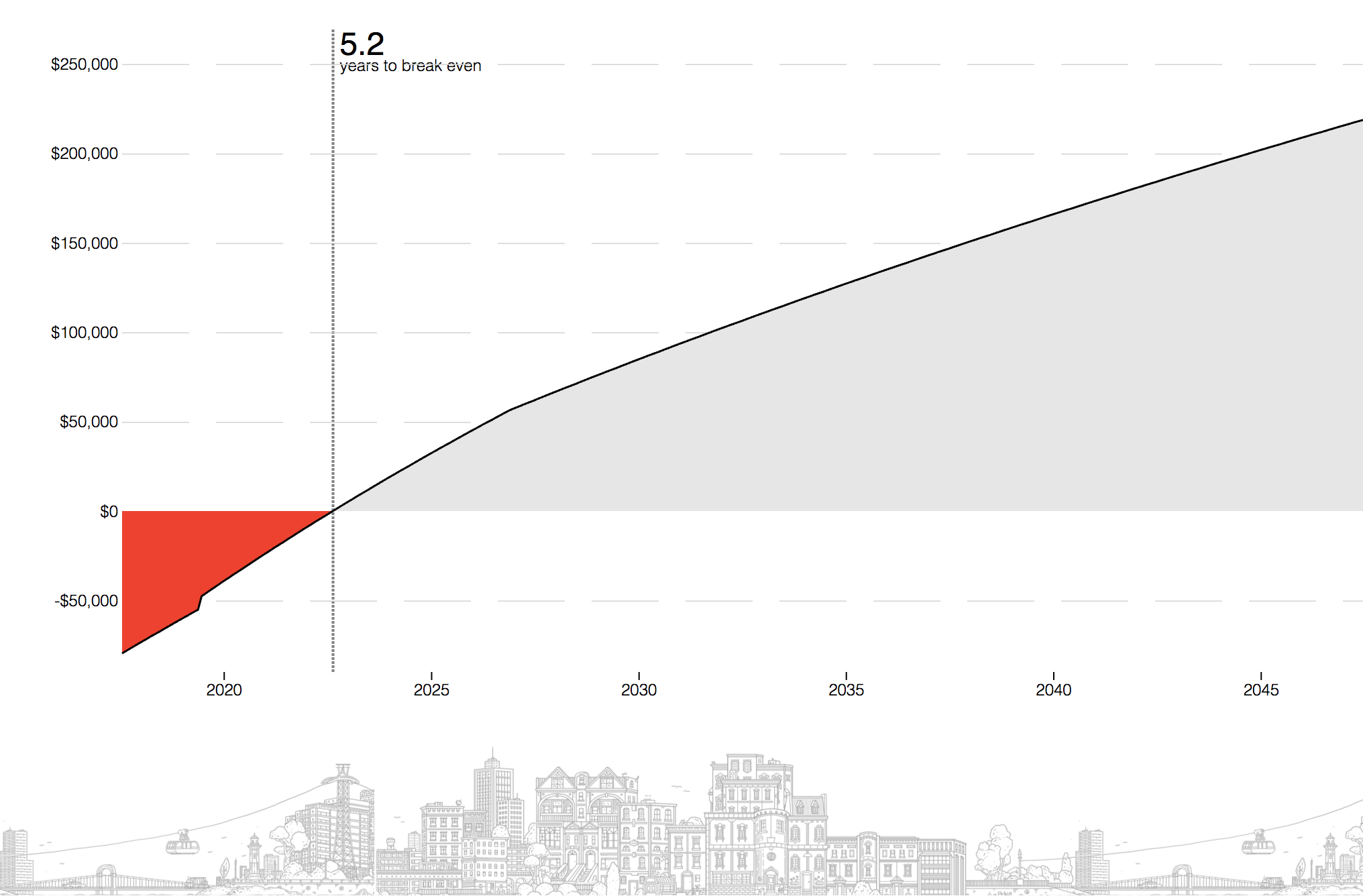

At StreetEasy, we call the point in time in which the benefits of owning a home exceed the benefits of renting that same home the tipping point. The median number of years required to break even on a home in New York City is 5.6 years, based on data from Q1 2017. That is up a full year from the same time period last year and is much higher than the nationwide median of just over 2 years. The longer time to break even on a home purchase in New York City is a direct result of higher home prices and rising mortgage rates, particularly when combined with falling rents. For New Yorkers not planning to spend more than 5.5 years in their new home, renting is, on average, a more attractive financial choice.

Since this time last year, tipping points increased in more than three-quarters (78 percent) of the 85 neighborhoods in New York City that we examined. The increases were most pronounced in more expensive areas of the city. The tipping point for Manhattan – the borough with the city’s priciest homes – had the largest increase over the prior year – up a year and half to 7.7 years. Tipping points for Brooklyn, Queens and the Bronx all increased by smaller amounts: 10, seven, and two months, respectively. Our analysis found the top 10 neighborhoods with the longest tipping points are concentrated in Manhattan, while the top 10 neighborhoods with the shortest tipping points are concentrated in the Bronx and Queens.

In the context of this analysis, the tipping point looks at the differences between renting and buying a specific type of unit in the same neighborhood. However, many New Yorkers eager to own a home in the city might consider moving to a less expensive area. For example, if a Manhattanite seeking to buy a one-bedroom is open to moving to Brooklyn or Queens in lieu of continuing to rent in Manhattan, they would face a tipping point of just 4.3 years or 1.8 years, respectively.

Find Your Tipping Point

Curious about your personal tipping point? We’ve created a new interactive tool to help you better understand what drives a tipping point in New York City and help you find your own based on your apartment size and the ideal neighborhood you’d like to own a home in.

The tipping point provides important context for current and future New Yorkers who are weighing the pros and cons of buying a home versus renting one. However, the profitability of homeownership depends on a wide range of factors that are impossible to predict with perfect precision, including the pace of future growth of home values and rents. Choosing to own a home is ultimately a personal decision, and New Yorkers should be mindful that both renting and buying have benefits and risks.

Over the coming months, we will continue to look at tipping points across New York City and how they change over time, and will also explore additional issues related to the economics and affordability of homeownership.

How We Did It

The tipping point is the earliest point in time at which the net present value of owning a home exceeds the net present of value of renting, a product of a cost-benefit analysis between the two. To determine the equivalent rent for each home for sale, we assign an equivalent rent for each condo and coop listed for sale on StreetEasy by matching the median rent for a unit in the same neighborhood with the same bedroom count.

Our tipping point calculations account for costs of both owning a home and renting a home, and considers the opportunity costs of investing upfront fixed costs such as a down payment, closing costs, and a security deposit in alternative assets such as stocks or bonds, net of taxes.

Costs of homeownership include mortgage principal and interest; applicable federal, state, and city taxes; homeowner’s insurance; projected closing costs; and maintenance fees and common charges as listed on StreetEasy. Homeownership costs are net of mortgage income tax deduction benefits. Costs of renting include brokers’ fees, renter’s insurance, and monthly rent. Tipping points for a given geographic area reflect the median value for all applicable units in that area. For the purpose of this analysis, we project home prices, rents, and alternative investments to grow in line with long term New York City averages. Neighborhoods and unit type combinations without a minimum of ten rental listings and ten sale listings were excluded from this analysis.