According to StreetEasy’s Q1 2022 market report, renters looking to sign a new lease this spring will encounter a competitive market driven by record-high rent prices, low inventory, and very few concessions.

In the first quarter of 2022, Manhattan asking rents were nearly $1,000 more per month than they were at the same time last year, reaching a record high of $3,695. In Q1 of 2021, the median asking rent was $2,700 – the lowest it’s ever been according to StreetEasy data, which stretches back to 2010.

Renters Facing Higher Prices Also Have Less to Choose From

On top of record-breaking monthly rents, finding an apartment is more difficult than it was last year. In Q1 2021, there were more than double the amount of available rental units than there were in Q1 2022. In Manhattan, 23,419 rentals were advertised on StreetEasy during the first quarter of this year. Last year there were 56,973 available during the same time period.

While this all sounds like bad news for renters, the latest data on rental inventory shows some promising signs. While inventory continues to fall, the declines from quarter to quarter are not nearly as steep as they were in 2020 and 2021. Between Q4 of last year and Q1 of this year, available rentals in Manhattan fell by 643. But between Q3 and Q4 of 2021, inventory had decreased by 16,426 – a significantly higher drop.

Manhattan Rentals Under $3,000 on StreetEasy Article continues below

We may even begin to see month-over-month increases in rental inventory available across the city. As of the week ending April 10, 2022, rental inventory has been increasing steadily for the past several weeks, and presently, StreetEasy is seeing the highest amount of rentals available since December.

Pandemic Deals Have Expired

At this time last year, it was significantly more common to come across a rental apartment offering a concession in the form of at least one month of free rent, particularly in Manhattan. During Q1 of last year, 42.8% of Manhattan rentals advertised a concession – the highest on StreetEasy record. Fast forward one year, and 13.1% of Manhattan rentals were offering a concession – a drop of nearly 30 percentage points. This was the lowest share of apartments offering a concession StreetEasy has seen since 2016.

With this shift in market dynamics, renters who signed a one-year lease at this time last year could face significant increases in monthly rent prices when their lease renewals arrive. If renters under those circumstances are forced to move, it would theoretically open up some inventory on the market. But if they choose to move elsewhere in the city, demand for lower priced rentals could spike even more.

Where Can Renters Go From Here?

“Renters can take this latest data as a sign to be prepared for their landlords to potentially present them a lease renewal with major increases. Having a plan for if and when that happens will be integral, whether you’re going to accept the increase or make some tradeoffs to find a more affordable space,” says Joshua Clark, Senior Economist at ZIllow.

“Renters are generally in a tougher position than they normally are this time of year, but those able to take over the lease on a pandemic-deal apartment may have more luck. There could be a mass exodus of renters priced out of their apartments in the coming months that could help alleviate the weaker than normal supply of rental inventory.”

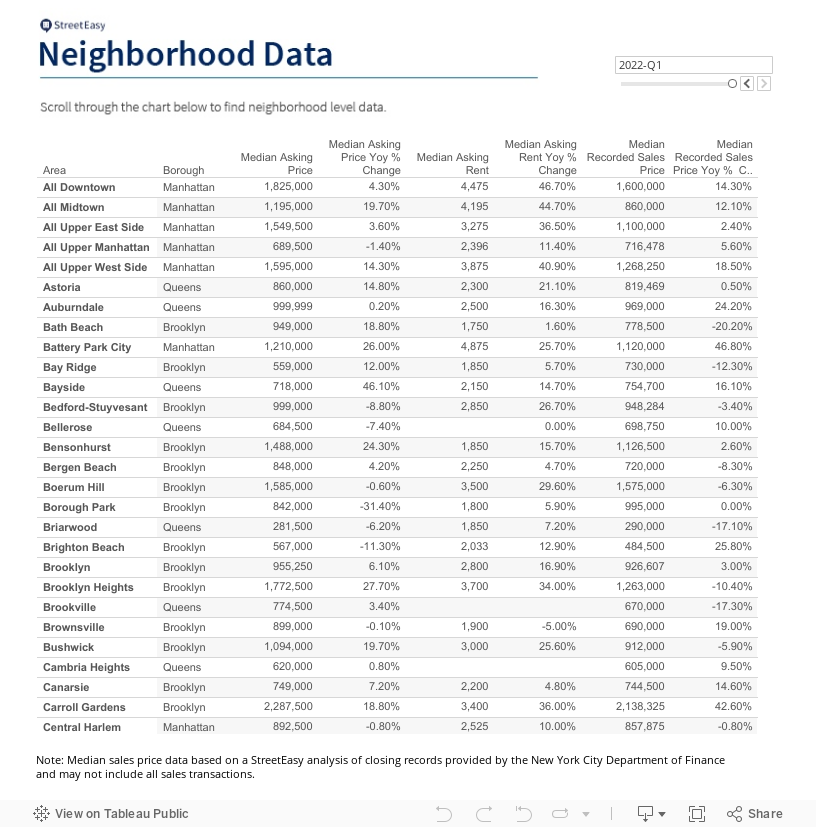

StreetEasy’s Data Dashboard is a great resource for renters looking to find neighborhoods within their budget. This interactive tool allows home shoppers to explore StreetEasy’s hyperlocal data and find median asking rents, inventory levels, the prevalence of concessions, and more on a neighborhood-by-neighborhood basis.

In this ultra-competitive market, renters should also ensure they’re notified as soon as new listings hit the market. When home shoppers save their searches on StreetEasy, they receive real-time alerts when new homes fitting their criteria hit the market – helping them find and win their home faster than the competition.

Find out more about the sale and rental markets in Manhattan, Brooklyn, and Queens below.

Manhattan Luxury Rentals See Lowest Price Growth

At $3,695 in Q1 2022, median asking rents in Manhattan were higher than ever before on StreetEasy record. The 36.9% year-over-year increase was also the most significant jump on StreetEasy record.

Luxury rentals in Manhattan (the top 20% of the market) saw the smallest year-over-year increases in rent, with a 23.6% jump to $6,844. Mid-tier rentals (the middle 40-60%) saw the largest year-over-year increase of 30%, reaching $3,516 in Q1.

Of all available rentals in Manhattan, 16.9% were discounted during the first quarter, down from 22.2% in Q1 2021.

Manhattan Homes Under $1.5M on StreetEasy Article continues below

On the sales market, Manhattan asking prices rose 7.7% to $1,395,000 during the first quarter. Inventory fell 10.1% year-over-year with 12,057 homes available on the market, but rose by 4% since Q4 2021. This is the first time in three quarters that there has been a quarterly increase in Manhattan sales inventory.

Brooklyn Rentals Offered The Fewest Discounts

Similar to Manhattan, Brooklyn asking rents reached a new high of $2,800 – up 16.9% from last year.

There were 21,863 units available for rent in Brooklyn in Q1, a 48% decrease from last year when 42,055 rentals were available. Still, the pace at which inventory is declining appears to be slowing in the borough.

Brooklyn Rentals Under $3,000 on StreetEasy Article continues below

Of the boroughs analyzed for this report, Brooklyn had the lowest share of rentals offering a discount in Q1 at 12%. That was down from 17.3% in Q1 2021.

On the sales market, Brooklyn asking prices rose 6.1% to $955,250 during the first quarter. Inventory fell 8.7% year over year with 6,668 homes for sale. Sales inventory remained relatively the same between Q4 2021 and the first quarter of this year, with 22 fewer homes available.

Queens Stands Out As Only Borough with Falling Prices & Rising Inventory

The median asking rent in Queens rose 15.1% year over year to $2,300 during the first quarter. The last time rents were this high was Q1 2020, just before the pandemic hit the city.

There were 9,825 rentals available in Queens in Q1, a 40.7% decrease from last year when 16,570 rentals were available. Queens inventory has remained relatively stable throughout the pandemic in comparison to Manhattan and Brooklyn.

Of the rentals available in Queens during the first quarter, 12.5% dropped their price while listed on StreetEasy. That was down from 17.8% in Q1 2021.

Queens Rentals Under $2,500 on StreetEasy Article continues below

On the sales market, Queens was the only borough analyzed to see a drop in prices and an uptick in inventory. Queens asking prices fell 3.2% to $599,000 during the first quarter, while inventory rose 2.8% year over year with 4,466 homes for sale.

For more data to help navigate the NYC home shopping process, view all StreetEasy Market Reports for Manhattan, Brooklyn, and Queens, with additional neighborhood data and graphics. Definitions of StreetEasy’s metrics, monthly data, and interactive charts from each housing market report can be explored and downloaded for free via the StreetEasy Data Dashboard.

Editor’s Note: In March 2020, New York City’s housing market temporarily froze as the COVID-19 pandemic reached the U.S. In 2021, the real estate market roared back to life, with demand returning to both the rentals and sales markets. Year-over-year data comparisons over the next few months will be made against the housing recovery that began in early 2021. Assuming 2022 is more typical of a “normal” year in housing than 2020 or 2021 were, with times of little to no activity followed by massive spikes in demand, we expect many of our year-over-year measures will show significant losses over last winter and spring. We urge you to use caution in extrapolating too much from year-over-year measures in the coming months, and we will always try to provide appropriate context to anchor reported changes in metrics to what is normal or expected.