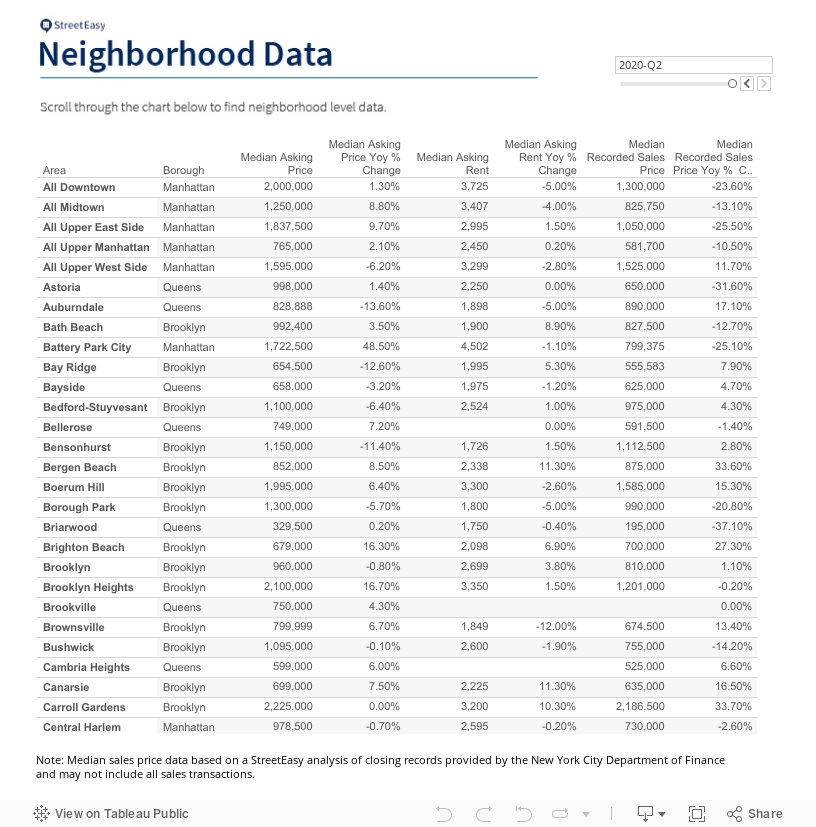

StreetEasy’s Q3 2019 Market Reports show Manhattan home prices falling to 2015 levels.

The number of homes for sale reached new highs in Brooklyn and Queens and jumped to near-highs in Manhattan, according to StreetEasy’s Q3 2019 Market Reports [i]. This latest data shows no imminent change to the gridlocked dynamics of New York City’s sales market, where stubbornly high asking prices, especially in Manhattan, have driven away many potential buyers.

The increase in for-sale inventory also means greater competition among home sellers. But those sellers are not responding with more price cuts: the share of listings with a price cut remained basically unchanged from last year. In Manhattan, this figure fell to its lowest level of 2019, with 23.7% of sellers offering a discount. The share of price cuts offered in Brooklyn rose just one percentage point to 22.3%, and it remained about the same in Queens, at 19.3%.

Nor are sellers willing to meet buyer demand with deeper discounts. The median size of price cuts in Manhattan, Brooklyn and Queens remained unchanged since last year, at 5.3%, 5.1%, and 4.3%, respectively.

Still further signs of a lagging sales market can be seen in price growth. In Manhattan, the StreetEasy Price Index [ii] fell 4.4% to $1,093,562 — its lowest level since 2015. In Brooklyn and Queens, price growth was essentially flat. These figures, calculated using data on home sales that closed, show that the sellers who priced their homes at more realistic levels were the ones who found buyers.

“Most sellers are still refusing to bow to the buckling market, causing would-be buyers to turn to the rental market, where they are finding a lot to like,” says StreetEasy Senior Economist Grant Long. “Until sellers recognize that prices are not what they once were, those with the means to buy will continue to play the waiting game from the comfort of their rental. With job growth in the city continuing to support demand for homes, we expect to see an unusually competitive winter in the rental market, including likely record rates of rent growth.”

See below for additional sales and rental market trends across Manhattan, Brooklyn and Queens.

Q3 2019 Key Findings — Manhattan

- A smaller share of homes received price cuts. While unchanged on an annual basis, the share of price cuts was the lowest in 2019 at 23.7%. The share of price cuts fell most in the Upper West Side [iii], down 4.1 percentage points to 22.8%.

- Prices dropped to 2015 levels. The StreetEasy Manhattan Price Index dropped to $1,093,562, a 4.4% decrease from last year. Prices fell the most on the Upper East Side [iv] — down 4.8% to $955,277.

- Sellers refused to offer larger discounts. The median price cut on homes in Manhattan was 5.3% of the asking price — unchanged since last year in all Manhattan submarkets.

- There were 915 more homes on the market. For-sale inventory increased 7.7% in Manhattan from a year prior, pushing the total number of homes for sale to just under 13,000.

- Rents rose at their fastest pace since 2015. The StreetEasy Manhattan Rent Index [v] rose to an all-time high of $3,318 – up 3.0% from last year.

Q3 2019 Key Findings — Brooklyn

- Price cuts on Northwest Brooklyn homes diminished. Boroughwide, the share of price cuts remained about the same. However, in Northwest Brooklyn [vi], one of the borough’s most expensive submarkets, the share of price cuts fell 3.1 percentage points to 17.2%.

- Prices remained the same. The StreetEasy Brooklyn Price Index remained stagnant at $699,813. In Northwest Brooklyn, prices fell 3.2% to $1,054,950.

- The median price cut remained unchanged year-over-year. Brooklyn sellers offered a median of 5.1% off their asking prices.

- Inventory reached an all-time high. Sales inventory increased the most in Brooklyn out of the three boroughs analyzed — up 12.4% from last year to 8,170 homes.

- Rents rose at the fastest rate in the city. The StreetEasy Brooklyn Rent Index jumped 3.9% from last year to $2,712 — the fastest rate in the city and the fastest in the borough since 2015.

Q3 2019 Key Findings — Queens

- Sellers offered the fewest price cuts. The share of price cuts offered by sellers was the same as last year at 19.3%, the lowest of all boroughs analyzed.

- Price growth slowed to 2013 levels. Prices in the borough remained stagnant at $510,499 — but overall price growth was the slowest in six years.

- Sellers offered the smallest discounts. Queens sellers cut a median of 4.3% from their asking prices, a level unchanged from last year.

- Sales inventory jumped to a record high. The number of for-sale homes increased 11.2% in the borough to an all-time high. In Northeast Queens [vii], inventory rose 19.9%, the most in the borough.

- Rents reached record highs. The StreetEasy Queens Rent Index increased 3.3% to $2,200, the most significant jump in rents in the borough since 2016.

Definitions of StreetEasy’s metrics and monthly data from each report can be explored and downloaded via the StreetEasy Data Dashboard.

[i] The StreetEasy Market Reports are a monthly overview of the Manhattan, Brooklyn and Queens sales and rental markets. Every three months, a quarterly analysis is published. The report data is aggregated from public recorded sales and listings data from real estate brokerages that provide comprehensive coverage of Manhattan, Brooklyn and Queens, with more than a decade of history for most metrics. The reports are compiled by the StreetEasy Research team. For more information, visit our Market Reports page. StreetEasy tracks data for all five boroughs within New York City, but currently only produces reports for Manhattan, Brooklyn and Queens.

[ii] The StreetEasy Price Indices track changes in resale prices of condo, co-op, and townhouse units. Each index uses a repeat-sales method of comparing the sales prices of the same properties since January 1995 in Manhattan and January 2007 in Brooklyn and Queens. Given this methodology, each index accurately captures the change in home prices by controlling for the varying composition of homes sold in a given month. Levels of the StreetEasy Price Indices reflect average values of homes on the market. Data on the sale of homes is sourced from the New York City Department of Finance. Full methodology here.

[iii] The Upper West Side submarket includes Lincoln Square, the Upper West Side, Manhattan Valley and Morningside Heights.

[iv] The Upper East Side submarket includes Lenox Hill, the Upper East Side, Yorkville, Carnegie Hill and Upper Carnegie Hill

[v] The StreetEasy Rent Indices are monthly indices that track changes in rent for all housing types and are currently available from January 2007 in Manhattan, January 2010 in Brooklyn, and January 2012 in Queens. Each index uses a repeat-sales method similar that used to calculate the StreetEasy Price Indices. The repeat method evaluates rental price growth based on homes in a given geography that have listed for rent more than once. More details on methodology here.

[vi] The Northwest Brooklyn submarket includes Downtown Brooklyn, Fort Greene, Brooklyn Heights, Boerum Hill, Dumbo, Red Hook, Gowanus, Carroll Gardens, Cobble Hill, Columbia St. Waterfront District and Clinton Hill.

[vii] The Northeast Queens submarket includes Bayside, Briarwood, Flushing, Kew Gardens, Kew Gardens Hills, Oakland Gardens and Whitestone.

—

Inspired to find your next place in New York? Whether you’re looking to rent or to buy, search NYC apartments on StreetEasy.