Overpriced homes are lingering on the for-sale market in New York City, according to the Q4 2018 StreetEasy Market Reports. (Getty Images/Busà Photography)

Last quarter, the number of homes for sale grew at double-digit rates in all five boroughs for the first time ever. In Manhattan, sales inventory rose 15.4 percent year over year, the fastest annual rate of growth in the fourth quarter since the financial crisis. As a result, fourth-quarter inventory was at its highest level since 2010, according to the Q4 2018 StreetEasy Market Reports [i]. Brooklyn and Queens also saw significant annual increases in inventory, up 22.0 percent and 30.8 percent, respectively.

Although the listing of new homes for sale slowed in the fourth quarter from the record highs reached earlier in the year, total inventory rose as overpriced homes lingered on the market. Homes that were fairly priced, however, sold in a similar timeframe as in 2017. Units that went into contract in Manhattan during the fourth quarter of 2018 spent a median of 86 days on the market, an increase of nine days from the previous year. In Brooklyn, homes took a median of 68 days to sell, down two days from the same period a year earlier. In Queens, homes spent 78 days on the market, just two days longer than in the fourth quarter of 2017.

“The glut of unrealistically priced homes in the city has been a main driver of the slow-moving market that ended 2018 — causing more and more homes to pile up before the new year and heightening competition among sellers,” said StreetEasy Senior Economist Grant Long. “Heading into 2019, sellers who are unwilling to budge on price are going to face an unforgiving market. Many sellers will have to make difficult pricing decisions in early 2019, particularly with another wave of inventory set to hit the market as the home-buying season heats up in the spring.”

See below for additional sales and rental market trends across Manhattan, Brooklyn and Queens.

Q4 2018 Key Findings — Manhattan

- Prices dropped for the fourth consecutive quarter. The StreetEasy Manhattan Price Index [ii] dropped 3.0 percent to $1,132,214, its lowest level since 2015.

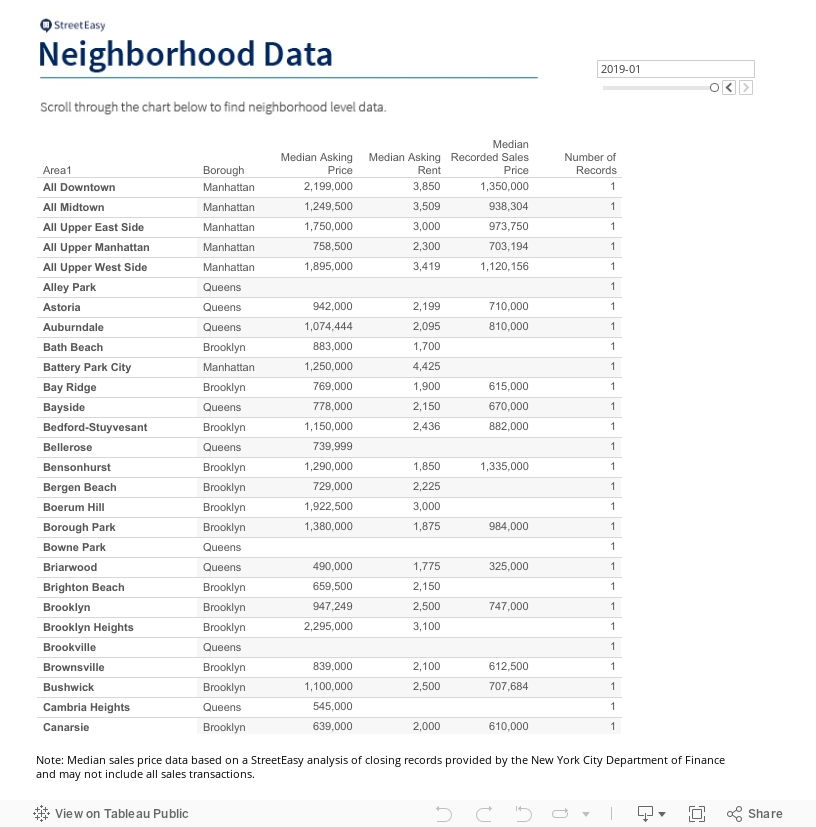

- The Upper West Side saw the lowest number of recorded sales since the financial crisis. There were 405 recorded sales [iii] in the Upper West Side [iv] in the fourth quarter of 2018 — a 23.7 percent annual drop.

- More than a quarter of homes had their price cut. The share of homes with a price cut in Manhattan increased by 4.9 percentage points year over year, reaching 26.8 percent. The median price cut amount remained unchanged, at 5.7 percent of the home’s total price.

- Rents rose in all submarkets. The StreetEasy Manhattan Rent Index [v] increased 2.4 percent annually, reaching $3,207. Rents rose the most in Upper Manhattan [vi], up 2.4 percent to an all-time high of $2,380.

- The share of units offering rental concessions dropped. In the fourth quarter of 2018, 9 percent of rentals in Manhattan offered a concession [vii], down 7.3 percentage points from last year — the largest annual drop since 2010.

Q4 2018 Key Findings — Brooklyn

- Prices rose after dipping briefly in the third quarter. The StreetEasy Brooklyn Price Index increased 2.6 percent annually to $711,578. Prices in South Brooklyn [viii] rose the most, reaching $724,055, an increase of 5.5 percent year-over-year.

- Recorded sales fell to 2012 levels. The number of recorded sales in Brooklyn dropped 18.8 percent annually, matching levels last seen in 2012.

- Homes came off the market two days faster. The median number of days on market dipped to 68 in Brooklyn, down two days from last year. Brooklyn was the only borough where median days on market dipped.

- Rents continued to climb. The StreetEasy Brooklyn Rent Index increased 1.5 percent to $2,584. Rents rose the most in Northwest Brooklyn, increasing 3.3 percent annually to $3,058.

- Only 1 in 10 rentals offered concessions. Concessions were harder to find in Brooklyn, with the share of units offering concessions down 8.7 percentage points from a year prior.

Q4 2018 Key Findings — Queens

- Prices continued to rise. The StreetEasy Queens Price Index increased 5.0 percent to $520,312. Home prices rose in every Queens submarket, led by growth in Central Queens [ix], where prices rose 6.9 percent to $539,006.

- There were more than 1,000 more homes on the market than in the fourth quarter of 2017. Total sales inventory increased 30.8 percent in Queens. Sales inventory jumped the most in Long Island City, on the heels of the Amazon HQ2 announcement — up 45.2 percent annually.

- More Queens sellers offered price cuts. The share of homes with a price cut rose 5.6 percentage points year-over-year to 19.3 percent in the borough. The median price cut amount remained unchanged at 4.5 percent.

- Rents reached an all-time high. The StreetEasy Queens Rent Index increased 2.6 percent annually, reaching $2,164.

- Landlords advertised concessions on fewer units. The share of rentals advertising concessions fell to 9.6 percent in Queens — down 5.6 percentage points annually.

View the complete StreetEasy Market Reports for Manhattan, Brooklyn and Queens, with additional neighborhood data and graphics. See definitions of StreetEasy’s metrics and monthly data from each report.

[i] The StreetEasy Market Reports are a monthly overview of the Manhattan, Brooklyn and Queens sales and rental markets. Every three months, a quarterly analysis is published. The report data is aggregated from public recorded sales and listings data from real estate brokerages that provide comprehensive coverage of Manhattan, Brooklyn and Queens, with more than a decade of history for most metrics. The reports are compiled by the StreetEasy Research team. For more information, visit https://streeteasy.com/blog/research/market-reports/. StreetEasy tracks data for all five boroughs within New York City, but currently only produces reports for Manhattan, Brooklyn and Queens.

[ii] The StreetEasy Price Indices track changes in resale prices of condo, co-op, and townhouse units. Each index uses a repeat-sales method of comparing the sales prices of the same properties since January 1995 in Manhattan and January 2007 in Brooklyn and Queens. Given this methodology, each index accurately captures the change in home prices by controlling for the varying composition of homes sold in a given month. Levels of the StreetEasy Price Indices reflect average values of homes on the market. Data on the sale of homes is sourced from the New York City Department of Finance. Full methodology here.

[iii] Recorded sales are projected for the period based upon 1) data received from the New York City Department of Finance through the final day of the period, and 2) historical seasonal trends.

[iv] The Upper West Side submarket includes Lincoln Square, Upper West Side, Manhattan Valley and Morningside Heights.

[v] The StreetEasy Rent Indices are monthly indices that track changes in rent for all housing types and are currently available from January 2007 in Manhattan, January 2010 in Brooklyn and January 2012 in Queens. Each index uses a repeat-sales method similar that used to calculate the StreetEasy Price Indices. The repeat method evaluates rental price growth based on homes in a given geography that have listed for rent more than once. More details on methodology here.

[vi] The Upper Manhattan submarket includes Hudson Heights, Hamilton Heights, Washington Heights, Inwood, Fort George, West Harlem, Central Harlem, East Harlem, Manhattanville, South Harlem and Marble Hill.

[vii] Concessions are defined as advertised, temporary price reductions in the form of one or more months of free rent. StreetEasy does not include non-traditional concessions, such as Netflix packages and discounted amenities. We also do not include the waiving of broker’s fees as concessions.

[viii] The South Brooklyn submarket includes Sunset Park, Bay Ridge, Dyker Heights, Bensonhurst, Bath Beach, Gravesend, Borough Park, Ocean Parkway, Kensington, Coney Island, Brighton Beach, Ditmas Park, Seagate, Flatbush, Midwood, Sheepshead Bay, Manhattan Beach, East Flatbush, Canarsie, Flatlands, Marine Park, Mill Basin, Bergen Beach, Old Mill Basin, Greenwood and Gerritsen Beach.

[ix] The Central Queens submarket includes Woodside, Jackson Heights, East Elmhurst, North Corona, Elmhurst, Corona, Maspeth, Middle Village, Ridgewood, Glendale, Rego Park and Forest Hills

—

Hey, why not like StreetEasy on Facebook and follow @streeteasy on Instagram?