StreetEasy’s rent vs buy calculator for NYC is called the Tipping Point, and it varies by borough and neighborhood. (Getty Images)

How do you know if makes sense to rent or buy in NYC? We’ve created a metric called the Tipping Point, which shows the number of years New Yorkers would have to live in a home for buying that home to become cheaper than renting it. The figure takes into account a number of market and macroeconomic factors (see below for our methodology) to weigh the costs of renting versus buying in NYC. Knowing the Tipping Point for where you want to live will help you decide whether it makes sense to become a homeowner here.

The Benefits of Homeownership vs. Renting

In New York City, it takes a median of 5.8 years for buying a home to become cheaper than renting one. That’s much higher than the national Tipping Point of just over two years. But to really know whether buying makes sense for you, look at the Tipping Point for the neighborhood where you want to buy, and then consider how long you plan to live there.

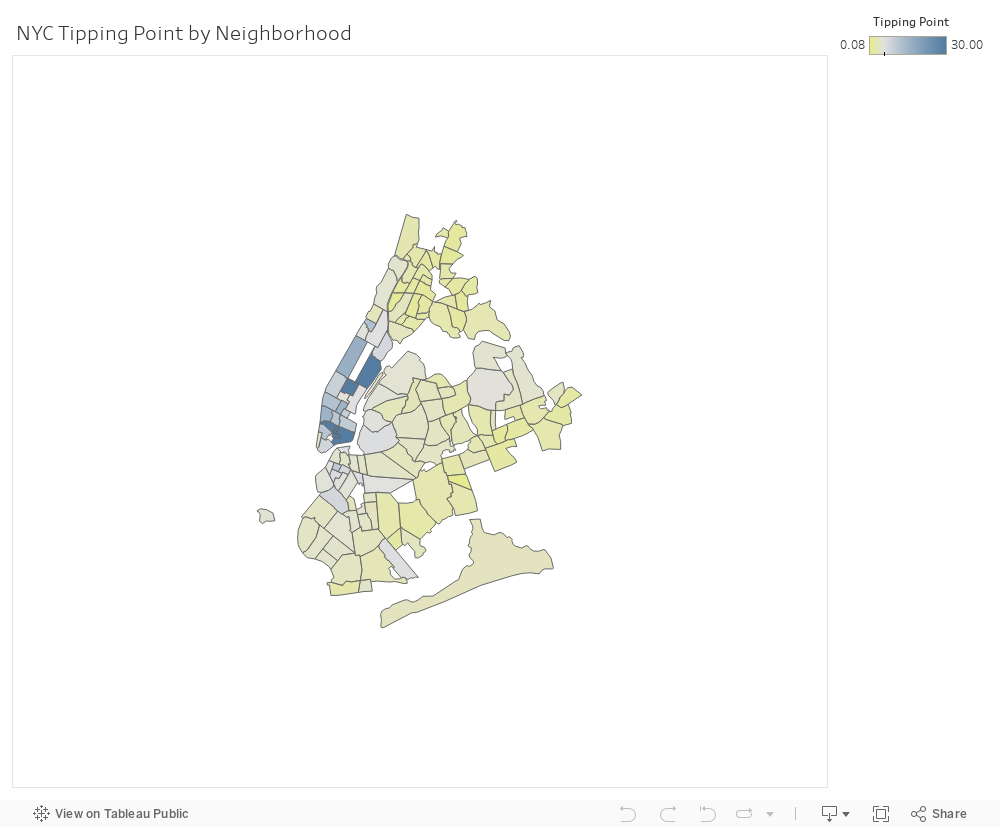

Hover over neighborhoods in the chart below to explore Tipping Points across the city:

Manhattan & Brooklyn Rentals Under $3,000 on StreetEasy Article continues below

Boroughs and Neighborhoods Impact Your Tipping Point

The Tipping Point ranges widely in NYC, from as many as 30 years in Manhattan neighborhoods like SoHo to less than three years in the Bronx. New Yorkers seeking to buy in Manhattan should be prepared to live in their home for a median of about 12 years to break even, while in Brooklyn and Queens, the median tipping point is around four years.

| Bronx | 2.33 |

| Brooklyn | 4.17 |

| Manhattan | 11.75 |

| Queens | 3.50 |

| Staten Island | 4.58 |

What If You’re Flexible About What Neighborhood to Live In?

There’s good news for buyers who have settled on a borough but are flexible about their neighborhood, since you can usually find a neighborhood next door to your first choice that has a lower Tipping Point. For example, buyers looking in Long Island City face a Tipping Point of five years. But if you’re open to Sunnyside, your Tipping Point would decrease to just over three years.

Note that this does not mean a neighborhood with a lower Tipping Point is better, or that one shouldn’t buy in Long Island City if one plans to stay a while. This metric is solely meant to show the time you’d have to live in a given NYC neighborhood for the financial cost of buying to be less than the cost of renting.

How the Tipping Point Works and What It Means

This Tipping Point metric weighs the costs of renting (monthly rent payments, brokers’ fees, and insurance) against the costs of buying. Those include the down payment, mortgage, property taxes, home maintenance costs — and the opportunity cost of investing the down payment and upfront fees in alternative assets, such as stocks and bonds. The model also takes into account rental and home value appreciation forecasts for each market, among other things.

Manhattan’s 11.8 year Tipping Point therefore does not mean that renting in Manhattan is cheap. It simply shows that because Manhattan’s home sale prices are so high, buyers there must pay bigger upfront costs, which take longer to recoup for the buyer to break even.

Manhattan & Brooklyn 1-2BRs Under $1M on StreetEasy Article continues below

Investments and Other Factors That Alter Your Tipping Point

Most of the factors that go into our Tipping Point — such as future mortgage rates, price appreciation, and stock market performance — are impossible to predict perfectly, and are out of a buyer’s control. However, your tipping point can vary with the size of your down payment.

Our model assumes a 20 percent down payment, the minimum requirement for most NYC co-ops. (Some co-ops require more, while condos often require less.) Renters who find a way to put down only 3 percent on a home in NYC will have a Tipping Point four months shorter than the median. Conversely, renters who pay all cash for a home here will face a Tipping Point 16 months longer than the median.

Here’s why that is: Renters who invest the money they would otherwise spend on a down payment and make at least a normal return of 5 percent per year on it will face a longer Tipping Point. Conversely, renters who do not save the money they would otherwise put into a down payment will see financial benefits of buying a home sooner, because their home becomes a savings vehicle.

Ultimately, of course, the decision to buy a home in NYC is a personal one. The StreetEasy Tipping Point is intended simply as a tool to help remove some of the financial guesswork.

How We Did It

The Tipping Point is the earliest point in time at which the net present value of owning a home exceeds the net present value of renting, a product of a cost-benefit analysis between the two. To determine the equivalent rent for each home for sale, we assign an equivalent rent for each condo and co-op listed for sale on StreetEasy by matching the median rent for a unit in the same neighborhood with the same bedroom count. Calculations are based on data from Jan. 1 to Nov. 15, 2019.

Our tipping point calculations account for the costs of both owning a home and renting a home, and consider the opportunity costs of investing upfront fixed costs such as a down payment, closing costs, and a security deposit in alternative assets such as stocks or bonds, net of taxes.

Costs of homeownership include mortgage principal and interest; applicable federal, state, and city taxes; homeowner’s insurance; projected closing costs; and maintenance fees and common charges as listed on StreetEasy. Homeownership costs are net of mortgage income tax deduction benefits. Costs of renting include brokers’ fees, renter’s insurance, and monthly rent. Tipping points for a given geographic area reflect the median value for all applicable units in that area. For the purpose of this analysis, we project home prices, rents, and alternative investments to grow in line with long-term New York City averages. Neighborhoods and unit-type combinations without a minimum of 10 rental listings and 10 sale listings were excluded from this analysis.

—

Inspired to find your next place in New York? Whether you’re looking to rent or to buy, search NYC apartments on StreetEasy.