The Federal Reserve Bank in Washington, D.C. Rising interest rates are one of several factors that will make buying NYC homes more difficult in 2018.

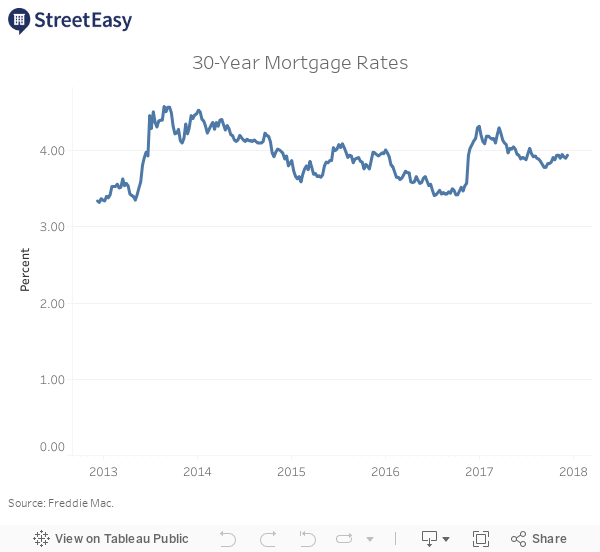

Today, the Federal Reserve voted to increase interest rates for the third time this year, a move widely anticipated by statements from Fed officials and last week’s strong jobs report. With the economy growing steadily, the Fed increased borrowing rates to help keep the pace of growth at sustainable levels. However, 30-year fixed mortgage rates have already risen in anticipation of this shift, and longer-term rates reacted little to today’s announcement.

This, of course, is a crucial issue for home buyers: For each quarter of a percentage point that 30-year mortgage rates increase, the monthly mortgage payment required to purchase a $750,000 home goes up nearly $90, adding $7,800 in total payments over the life of the loan.[1] Understandably, then, home buyers tend to get nervous on days like today, when it becomes clear that rates will continue to rise in the near term.

Why Today’s Federal Reserve News Matters to New Yorkers

Buying a home in New York City already grew less attractive compared to renting over the last year, as prices in the city’s most affordable neighborhoods surged. At StreetEasy, one way we gauge the favorability of buying over renting is the amount of time a New Yorker needs to stay in their home for buying to make financial sense. We call this measure the tipping point, and find that on average, as of the third quarter of 2017, New Yorkers should plan to spend 6.3 years in their new home for buying to pencil out. This is eight months longer than the tipping point from the same period last year — in part because of price dynamics, but also due to the ongoing increases in mortgage rates.

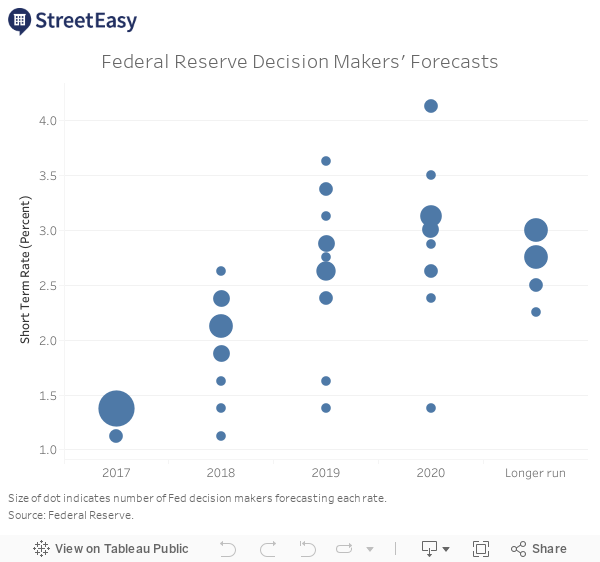

Yet while the Federal Reserve’s decisions play a key role in determining 30-year mortgage rates over long periods of time, decisions like the one announced today have little immediate effect on mortgage rates. Often, the Fed negotiates interest rate decisions weeks or months in advance. Federal Reserve Board Chair Janet Yellen and others previewed today’s move in speeches and interviews. Fed decision makers publish forecasts of future rates quarterly, and importantly, their forecasts for future rates and economic growth also went up today.

Washington Set to Drive a Bumpy Ride for Rates in 2018

Those planning to finance a new home purchase should worry more about policies coming out of the White House and Congress than the Federal Reserve. While the Fed prides itself on the predictability of its policies, the late-night drama of the recent tax reform effort shows that the political nature of other branches of the government leads to outcomes that are far harder to forecast. Adjustments to capital gains taxes and the deductibility of property taxes and mortgage interest could have a far greater effect on the attractiveness of homeownership than interest rate fluctuations. Proposed tax reforms are already putting upward pressure on interest rates, as the Fed adjusts its forecasts for the wave of new money this legislation would throw at the economy — and reacts more forcefully than it would without such a tax bill. Recall that the largest jump in 30-year mortgage rates since 2013 came last November, as a reaction to an unforeseen political event: the election of Donald Trump as president.

A number of changes are coming to the Fed that could cause further headaches for home buyers. Jerome Powell is set to replace Janet Yellen as chair early next year, and numerous other key posts at the Fed are either vacant or set to turn over. A wave of new Fed officials could result in adjustments to the way the Fed approaches its interest rate policy, or even a new approach to the $1.8 trillion of mortgages the Fed bought during and after the financial crisis. When the Fed surprised markets in June 2013 by announcing a shift in how many mortgages it was willing to purchase, mortgage rates jumped more than half a percentage point.

With Mortgage Rates Rising, Expect New Yorkers to Head to the Outer Boroughs

New Yorkers seeking to buy affordable homes had a rough year in 2017, and policies in Washington are likely to make buying even more difficult in 2018. As we highlighted in our predictions for the upcoming year, we expect more seekers of affordable homes to head to the outer boroughs. Our analysis shows that trading an expensive, central locale for a more distant one can make buying much more attractive. To illustrate how switching neighborhoods can benefit buyers in 2018, we’ve updated our interactive tipping point feature to allow users to explore the benefits of moving.

For more details on the calculations underlying StreetEasy’s tipping point, see our analysis from June.

[1] Monthly payment figure assumes a 20 percent down payment on $750,000 home. Total payments figure assumes homeowner does not prepay mortgage.

—

Hey, why not like StreetEasy on Facebook and follow @streeteasy on Instagram?

Related: