![[header] nyc rental inventory - skyline image](https://www.zillowstatic.com/bedrock/app/uploads/sites/26/header-nyc-rental-inventory-skyline-image-bf63d6.jpg)

It’s been a tumultuous 18 months in the New York City rentals market. Recently, as renter demand came roaring back, record low rents jumped back up to just shy of their pre-pandemic highs. Since last October, as rents rose, NYC rental inventory was on a downward trajectory. It now sits at 30,326 rentals available on StreetEasy — that’s a 59% decrease from October 2020, when there were 74,078 rentals available.

Table of Contents

- NYC Rental Inventory Plummets, Especially in Manhattan

- Brooklyn and Queens Rental Inventory Also Drops

- Studio Apartments Are Lagging Behind the Recovery

- Why Manhattan’s Rental Trends Are Different

- Downtown Manhattan Rents Hit Record High

- Brooklyn Rents Still Just Shy of Pre-Pandemic Highs

- In Queens, For-Sale Home Prices Drop While Rents Rise

Manhattan Rentals Under $3,000 on StreetEasy Article continues below

NYC Rental Inventory Plummets, Especially in Manhattan

NYC rental inventory is particularly down in Manhattan. In October, there were 13,048 Manhattan rentals available on StreetEasy. That is the lowest since December 2012 (excluding an anomaly in April 2020, directly after the pandemic put New York real estate temporarily on pause). And the drop in inventory was significant, falling 68.3% from where it was just one year ago.

Brooklyn Rentals Under $3,000 on StreetEasy Article continues below

Brooklyn and Queens Rental Inventory Also Drops

Compared to Manhattan, Brooklyn and Queens rental inventory is less volatile. It hasn’t dropped as dramatically in comparison to the pandemic highs, when a record number of apartments were available. But the changes are still significant.

In Brooklyn, rental inventory was down 53.7% from last October (compared to 68.3% in Manhattan) to 11,150 rentals. In Queens, inventory was down 34.5% from last October to 5,186.

Queens Rentals Under $3,000 on StreetEasy Article continues below

Studio Apartments Are Lagging Behind the Recovery

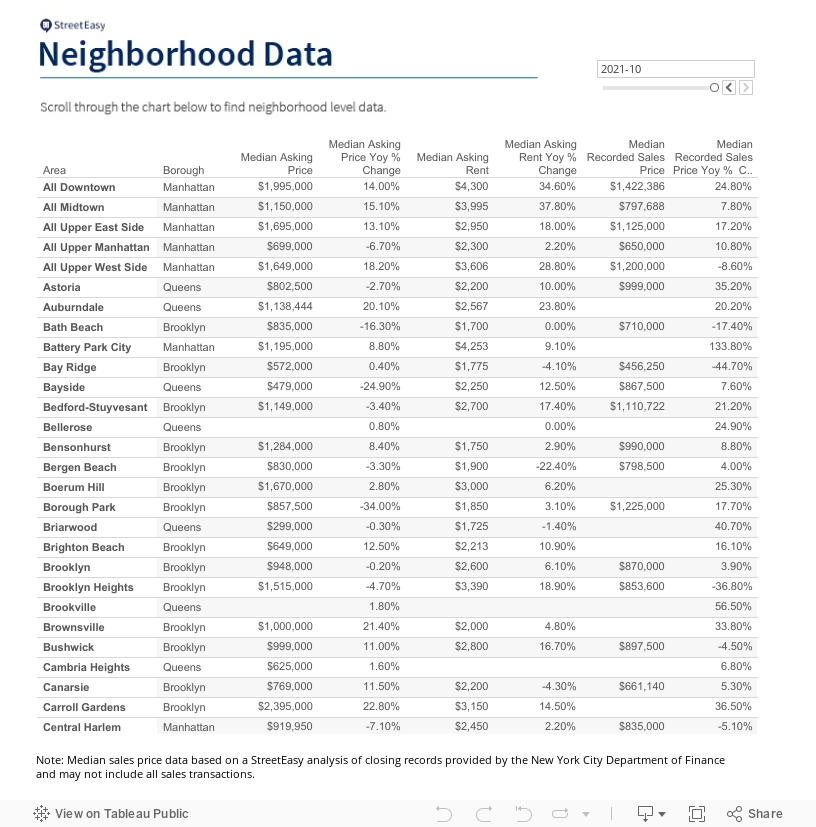

Our latest data shows that rents are recovering quickly across the city — and they’re rising the most in Manhattan. The median asking rent in Manhattan in October was $3,330, just $200 shy of the pre-pandemic high of $3,500.

With that said, not all apartment types are experiencing the same increases. Studio apartments have had the slowest recovery in rents month-over-month since the beginning of the year, across all boroughs analyzed. But the difference is the most stark in Manhattan.

The median asking rent for a Manhattan studio in October was $2,400 — a 14.6% increase from last year, when it was $2,095. This is a significant rise, but it’s much smaller than, say, 2-bedroom apartments, which saw a 25.4% annual increase from $3,350 to $4,200.

According to StreetEasy economist Nancy Wu, shifting priorities as a result of the pandemic have likely played a role in studios lagging behind. “Renters want more space after more than a year cooped up in their small apartments,” Wu says. “For many, remote work has brought about some cabin fever. And for those who are able to afford it, adding an extra bedroom or more space in general is a priority.”

Why Manhattan’s Rental Trends Are Different

Wu says this is likely because of different trends seen across the city during the pandemic.

“Transient Manhattan renters were most likely to leave the city, either temporarily or permanently, during the height of the pandemic,” she explains. “That drove the highest share of rental vacancies in Manhattan among the boroughs. It’s why we’re now seeing Manhattan’s inventory experience bigger swings and more dramatic changes as it recovers — because it saw the biggest shift away from what a normal market would look like.”

The big drops in NYC rental inventory make for a competitive rentals market right now. Wu expects it to continue for the next several months, even during the typically slow winter season. If you’re in the market to rent, check out our top tips on how to maximize your search and the recap of our recent Insider’s Guide to Renting webinar.

Read on for more on the latest in Manhattan, Brooklyn, and Queens.

Downtown Manhattan Rents Hit Record High

- The median asking rent in Manhattan in October was $3,330, up 17.9% from last year, when rents were at $2,800. In Downtown Manhattan, rents hit a record high $4,300 in October.

- The share of apartments with a discount on rent was 16.0% in Manhattan — down from 28.7% last year.

- The median asking price of for-sale homes in Manhattan was $1,487,500 — up 10.2% from last October.

Brooklyn Rents Still Just Shy of Pre-Pandemic Highs

- The median asking rent in Brooklyn was $2,600 in October — 6.1% higher than one year ago, but still a bit lower than the pre-pandemic highs around $2,700.

- The share of apartments with a discount on rent was 11% in Brooklyn — down from 23.8% last year.

- The median asking price of for-sale homes in Brooklyn was $948,000 — remaining stagnant from last year.

In Queens, For-Sale Home Prices Drop While Rents Rise

- The median asking rent in Queens was $2,250 in October — 7.1% higher than one year ago.

- The share of apartments with a discount on rent was 10.5% in Queens — the lowest share of all boroughs analyzed. That’s down from 20.7% last October.

- The median asking price of for-sale homes in Queens was $599,000 — down 6.6% from last year.

View all StreetEasy Market Reports for Manhattan, Brooklyn, and Queens, with additional neighborhood data and graphics. Definitions of StreetEasy’s metrics and monthly data from each report can be explored and downloaded via the StreetEasy Data Dashboard.

Editor’s Note: In March 2020, New York City’s housing market temporarily froze as the COVID-19 pandemic began in the U.S. in earnest. Stay-at-home orders were widespread. Year-over-year data comparisons over the next few months will be made against both the COVID freeze of the spring, and subsequent housing recovery that began last fall. Assuming 2021 is more typical of a “normal” year in housing than 2020 was, with little to no activity in the spring and summer, we expect many of our year-over-year measures will show large gains over last spring and summer. We urge you to use caution in extrapolating too much from year-over-year measures in coming months, and we will always try to provide appropriate context to anchor reported changes in metrics to what is normal or expected.