Conventional wisdom tells us that if you plan to live in your next home for 50 years, it makes sense to buy. Conversely, if you plan to live in your next home for just six months, it probably makes more sense to rent. But the large gray area in between those times frames makes he decision to buy or rent a difficult one, especially in a market as expensive and competitive as New York City. Many renters may feel that homeownership in the Big Apple is a pipe dream, with the common perception that renting is the only viable option in the face of prohibitively high home sale prices. At what point in time does buying over renting become a true toss-up in New York City?

To answer this question, we’ve developed the StreetEasy Tipping Point, a new metric which approximates the number of years it would take for the costs of owning a home to equal the costs of renting a comparable one in the same area. Our findings suggest that it makes financial sense to own a home in New York City instead of renting if a person intends to stick around for longer than 4.9 years – a much shorter time than many New Yorkers may expect.

Of course, every New York City neighborhood is different and some of the more expensive areas of Manhattan and Brooklyn carry a much longer tipping point. On the whole, however, the majority of New York City neighborhoods are accessible to aspiring buyers in five years or less.

The (Complicated) Cost-Benefit Analysis, Explained

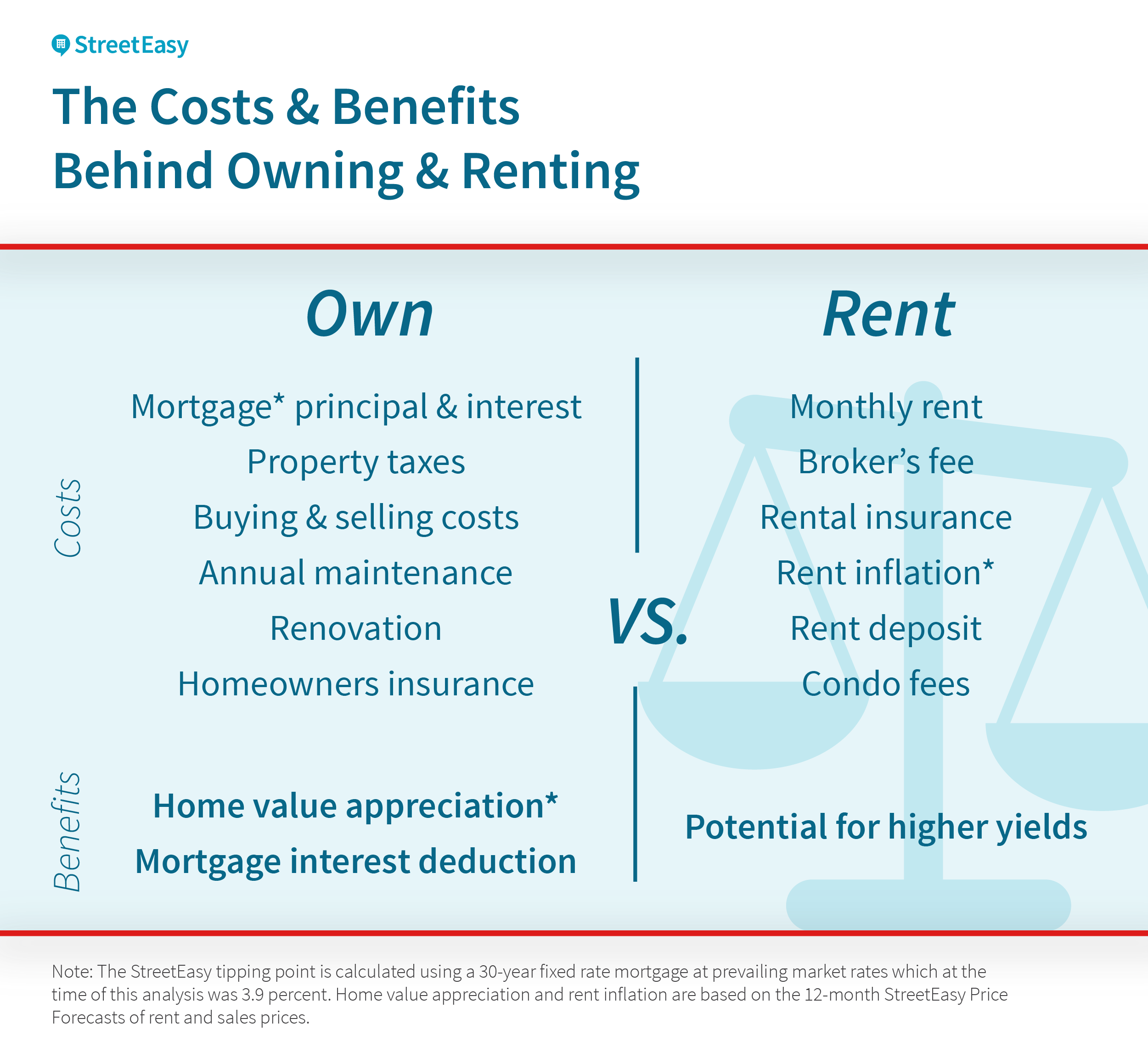

The decision to buy or rent is really a choice between two options: investing in an appreciating asset (a home), or freeing your money for other, potentially higher-yielding investments. Each of these options have their own costs and benefits and the tipping point includes many of them to calculate the number of years in which the accumulating net costs of renting would exceed the costs of buying. In other words, if you plan to live in a place for longer than the tipping point, it would make financial sense to buy a home rather than to rent a comparable one.

In the chart above, some of the costs and benefits of owning and renting are listed. Among the major benefits to homeownership is home value appreciation: Your home is likely to be worth more in the future than it is today. In Manhattan, for example, the median resale price of all homes rose 31 percent between 2005 and 2015, according to the StreetEasy Price Index. All things being equal, higher home value appreciation lowers an area’s tipping point since the costs of homeownership are more quickly recouped by the growing value of the home. Conversely, low or negative home value appreciation lengthens an area’s tipping point.

It is often said that renting is akin to throwing money out the window, but it does come with a considerable financial benefit: the ability to direct your savings toward other uses. New York City is home to more than a few Wall Street mavens who may be able to get a higher return on investments outside of local residential real estate. For these investors, the tipping point might be very high: Their yield on an alternative investment outweighs local home value growth and they may be quite satisfied to remain renters.

Living in New York City for More Than 5 Years? Think About Buying

When factoring these costs and benefits, we found that the median tipping point in New York City is 4.9 years. Among the five boroughs, the tipping point is longest in Manhattan (7.4 years), followed by the Bronx (4.6 years), Brooklyn (4.4 years), Staten Island (4.1 years) and Queens (3.0 years).

To put this into context, Zillow produces a similar metric to track the breakeven point across the United States and in every metro region. In Q4 2015, the breakeven point in the U.S. was 1.9 years, less than half the time it takes in New York City according to StreetEasy’s analysis.

Just as there is variation between boroughs, so too is there variation within them. Neighborhoods in Manhattan have a wide range of tipping points, with 24.4 years needed in West Chelsea compared to just 1.4 years in Roosevelt Island. In Brooklyn, neighborhoods in East Brooklyn often have a tipping point of less than two years, while Boerum Hill has a tipping point of 16.4 years. Queens has a smaller range of neighborhood tipping points, going from 1.1 years in Alley Park to 6.5 years in Douglaston. Belmont in the Bronx has the lowest tipping point in the borough at 1.6 years, while it is 18.5 years in City Island. Staten Island has a wide range of tipping points, from 19.2 years in Randall Manor to just 2.1 years in Clifton.

In some neighborhoods, the combination of prohibitively high asking rent and sales prices along with a relatively high median down payment result in a tipping point of over 30 years, meaning the homeowner will need to repay the mortgage before reaching the tipping point. These neighborhoods are largely concentrated in Manhattan, and include Carnegie Hill, Little Italy, Nolita, Soho and Tribeca.

How We Did It

The tipping point is the product of a cost-benefit analysis between two options: homeownership and renting. To calculate the homeowner’s side, starting with recorded sales prices and asking prices for properties in the city, we account for the costs of purchasing, owning and selling each home. We also calculate the costs of the 30-year fixed rate mortgage, its mortgage interest tax deductions and the tax implications of selling the home. We factor in the New York City mortgage tax and the mansion tax, when applicable (sales priced above $1 million are subject to the city’s mansion tax). Then we use the median down payment percent for the area and the likely home price appreciation using the StreetEasy Price Forecast of the appropriate borough. This allows us to calculate the homeowner’s expected return for each property.

Next, we calculate the renter’s side for the same property. First, we determine the likely asking rent of the property, given the area and number of bedrooms, using StreetEasy’s rental listings of comparable properties. We use the StreetEasy Rent Forecast of the appropriate borough to adjust for rent inflation. We include a broker’s fee adjusted for the likelihood of paying a fee. We assume a rental insurance rate of 1.32 percent and a deposit of one month’s rent. We also assume that the down payment would earn an annual return of five percent, and adjust for taxes.