Key Takeaways:

- The recent 0.8 percentage point decline in mortgage rates means a buyer looking for a starter home in NYC can see their purchasing power increase by nearly $71,000.

- This additional buying power would increase the number of affordable homes on the market by 7.4% across NYC. In Manhattan, buyers would see a 14.1% increase in homes within budget.

- Seller concessions can also increase the number of homes that are affordable to buyers. To date this year, 2.3% of homes for sale offered concessions, a notable increase from 1.4% on average in 2021.

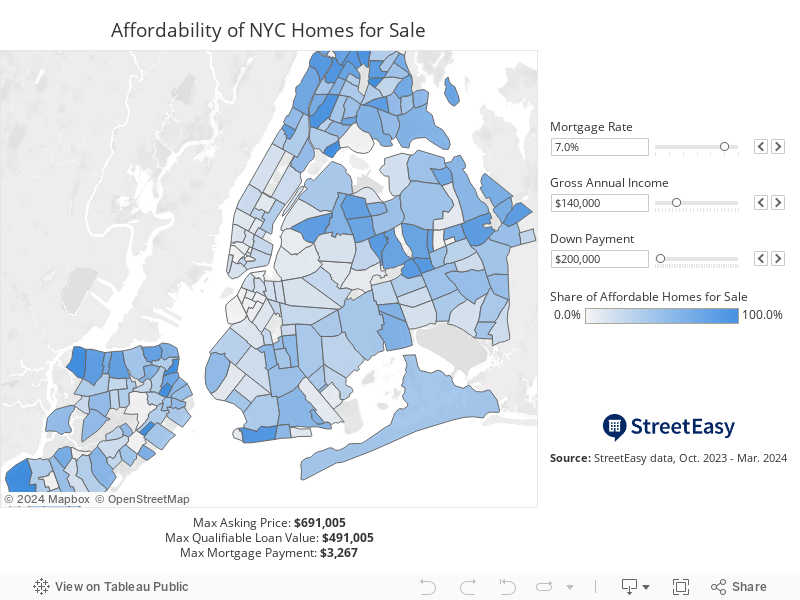

- For a wide range of budgets, there are opportunities for buyers across the city. Our interactive map lays out the share of homes within reach by neighborhood based on a buyer’s maximum budget, determined by their income, down payment, and mortgage rate.

Mortgage rates have been declining for several months and will likely hit 6% by end of year, as inflation continues to cool and the Federal Reserve eventually cuts interest rates. In the meantime, expect mortgage rates to fluctuate within the 6-7% range, significantly impacting the budgets of would-be home buyers.

A lower mortgage rate means buyers can secure a larger loan while keeping their down payment and monthly mortgage payments the same, allowing them to afford more homes. Conversely, a jump in rates would reduce their purchasing power, putting scores of homes out of reach.

Manhattan Homes Under $1M on StreetEasy Article continues below

For example, between October and March, the average 30-year fixed mortgage rate dropped from 7.6% to 6.8%. Over the same period, the citywide median asking price of a one- or two-bedroom home was $850,000 — a typical price point for a starter home in NYC. With the 0.8 percentage point decrease in mortgage rates, a buyer with this budget and a $200,000 down payment would be able to increase their purchasing power by nearly $71,000 — without raising their down payment or monthly mortgage payments.

Across NYC, for the same hypothetical buyer, this additional buying power would increase the number of homes affordable to them by 7.4%. In Brooklyn and Queens they’d have 5.1% and 3.7% more options, respectively, in addition to the homes that were already within reach. In Manhattan, buyers would see 14.1% more homes within budget — helping them unlock even traditionally more expensive neighborhoods.

Down Payment, in Addition to Mortgage Rates, Affects Affordability

The first step in understanding affordability is assessing how much a buyer can put down. In NYC, most co-ops require at least 20% of the sale price to be paid in cash, while condos can be more flexible. Among buyers who relied on mortgages for home purchases, the median ratio of mortgage amount to sale price, called the loan-to-value (LTV) ratio, was 75% in NYC in 2022 according to Home Mortgage Disclosure Act (HMDA) data, meaning the typical down payment was 25%. Since then, elevated mortgage rates and high asking prices suggest NYC buyers have relied even less on mortgages this year and last.

Putting down more than 20% has many advantages, including lower mortgage rates and a headstart on building equity. In a competitive market, an offer with more cash upfront can have an advantage over those of other buyers. Even if an offer isn’t all-cash, sellers may prefer an offer with a higher down payment, as it involves less risk of the contract falling through due to mortgage contingencies. Moreover, most lenders require mortgage insurance if buyers put less than 20% down, creating an additional monthly cost.

Brooklyn Homes Under $1M on StreetEasy Article continues below

Even a Small Drop in Mortgage Rates Can Make a Big Difference

After securing a down payment, buyers should understand the monthly mortgage payment they can afford relative to their income. Conventional wisdom says buyers should aim to keep mortgage payments and other monthly housing expenses below 28% of their monthly gross income. Buyers with other debts (car loans, student loans, credit card debt, etc.) should aim to keep their total monthly debt servicing burden, including mortgage payments, below 36% of their monthly gross income. This is often referred to as the 28/36 rule for home affordability.

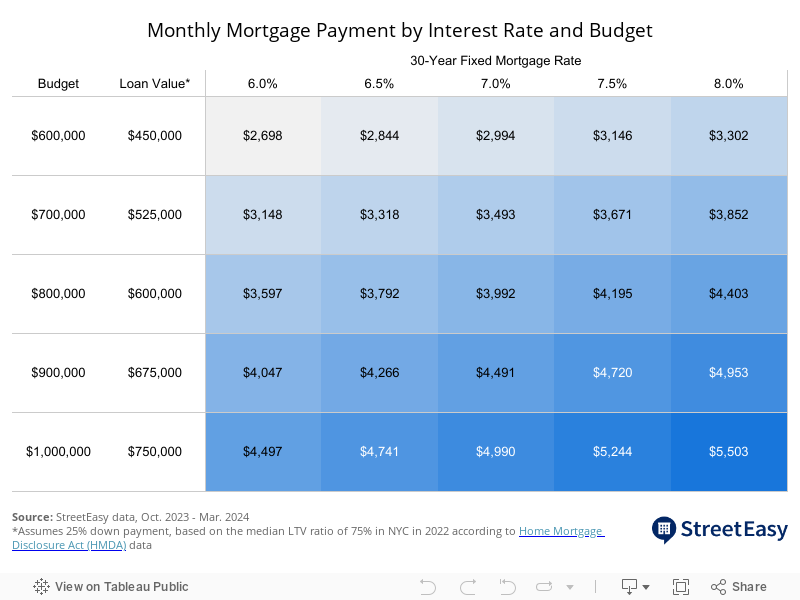

For example, an NYC buyer with an $800,000 budget and 25% down payment would need a $600,000 mortgage to purchase their next home. The expected monthly payment for this mortgage financed at 7% would be $3,992, which requires the buyer to earn at least $171,085 in gross annual income to keep their housing payment burden below 28%. If the same mortgage were financed at 7.5%, the monthly payment would increase by $203 to $4,195, requiring the buyer to earn at least $179,786 in gross annual income. The table below shows monthly mortgage payments for different loan values financed at various rates.

At a 7.5% rate, should this buyer wish to keep their monthly mortgage payment at $3,992 — ensuring housing and mortgage expenses stay below 28% of their monthly income — the buyer would have to pay $29,100 more upfront to reduce the loan value, or lower their budget by the same amount.

Conversely, a drop in mortgage rates would make it possible for buyers to qualify for larger loans while maintaining the same monthly payment. A decrease from 7% to 6.5%, for instance, would allow the same buyer to increase their budget by $31,548 and afford more homes on the market.

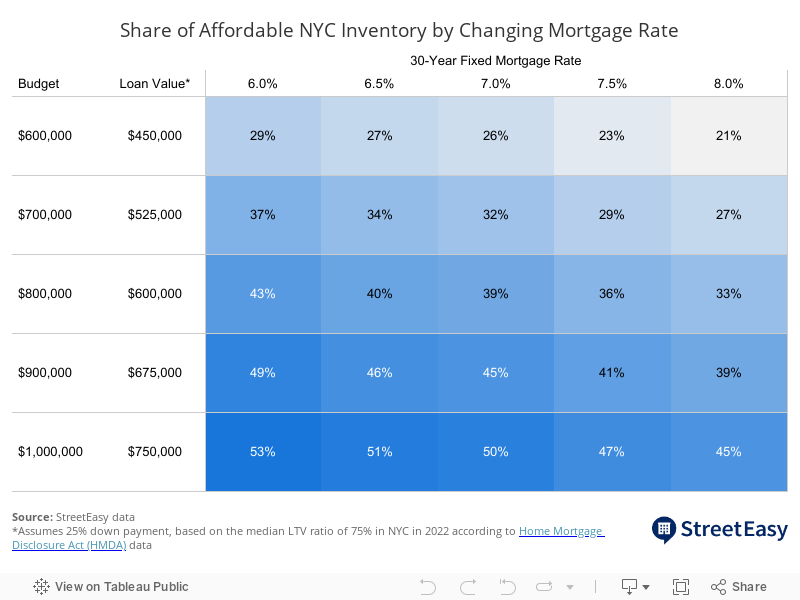

Changing budgets driven by shifting mortgage rates have a substantial effect on the share of inventory that buyers can afford. At 7%, the buyer with an $800,000 budget and 25% down payment can afford 39% of homes currently on the market in NYC, StreetEasy® data shows. If rates were to drop to 6%, the same buyer’s share of affordable homes would rise to 43%. Similarly, a buyer with a $1M budget would see their share of affordable inventory rise from 50% to 53% when rates drop from 7% to 6%.

However, it’s important to note that our calculation does not guarantee the rates and expected monthly payments buyers may encounter in the market. Depending on many different factors unique to each buyer, borrowers can make various adjustments to their mortgages that result in significant savings per month and over the lifetime of the loan. When shopping for a mortgage, be sure to speak to a qualified mortgage professional and compare quotes from multiple lenders.

What Can You Afford With Your Budget?

What buyers can afford ultimately depends on their down payment, and the maximum amount of mortgage they can qualify for based on their interest rate and annual income. Based on these criteria, the interactive map below lays out the share of NYC homes that would be within reach by neighborhood. Put in your mortgage rate, gross annual income, and down payment to see your results — including the maximum asking price you can afford, maximum monthly mortgage payment, and maximum qualifiable loan value. The latter follows the 28/36 rule, and we assume the maximum LTV ratio is 80%.

Negotiating Affordability Beyond Rate and Home Price

Beyond mortgage rates, down payment, and price of the home, buyers can further expand their affordability by negotiating for seller concessions. Seller concessions have been on the rise in NYC as a way for sellers to attract more home shoppers without reducing asking prices. These concessions typically help reduce closing costs for buyers. To date this year, 2.3% of homes for sale offered concessions, a notable increase from 1.4% on average in 2021.

A common seller concession is called a rate buydown, in which buyers pay upfront for mortgage “points” (referring to a percentage of the loan value) in exchange for a reduced mortgage rate. This results in lower monthly mortgage payments for the first few years of the loan, or sometimes permanently. It can save the buyer substantial amounts on interest over the lifetime of the mortgage, which makes a rate buydown more attractive when the buyer plans to own the home for a long time. Generally, NYC buyers are more likely to find concessions among sponsor units. This year, 2.1% of sponsor condos offered rate buydowns, a significant increase from 0.1% on average in 2021.

Queens Homes Under $800K on StreetEasy Article continues below

Resources for Borrowers

In this market, where even a small break in mortgage rates or down payment can have a significant impact on purchasing power, NYC buyers should find out if they qualify for mortgage assistance. These city, state, and federal programs offer lower interest rates, down payment assistance, or even help with closing costs. For instance:

- The State of New York Mortgage Agency (SONYMA) provides several options for qualified buyers, with 3% down payment assistance and rates as low as 6.125% within programs such as Achieving the Dream, Low Interest Rate, and Homes for Veterans.

- HomeFirst, a city program, provides first-time buyers making up to 80% of the area median income with as much as $100,000 toward their down payment or closing costs.

For more programs and information, see our article on 10 Mortgage Assistance Programs First-Time Home Buyers Should Know About.

No matter your financial situation, the licensed StreetEasy Concierge is available to give complimentary, personalized guidance on finding and buying a home in NYC within your budget. Connect with the Concierge to discuss everything from affordability to the buying process to current market trends. When you’re ready to buy, they’ll even match you with a top buyer’s agent from StreetEasy’s Experts Network, who can provide local market expertise and negotiate on your behalf to get the best possible deal.

Get help finding the best home for your budget

CONNECT WITH THE CONCIERGEStreetEasy is an assumed name of Zillow, Inc. which has a real estate brokerage license in all 50 states and D.C. See real estate licenses. All data for uncited sources in this presentation has been sourced from Zillow data. All third-party product, company names and logos are trademarks of their respective holders and use of them does not imply any affiliation. Copyright © 2024 by Zillow, Inc. and/or its affiliates. All rights reserved.