On Wednesday, the Federal Reserve raised interest rates by 0.75 percentage points. Consecutive hikes of 0.75 percentage points in June and July, following a half point increase in May, underscore the Fed’s willingness to deliver strong responses to fight elevated inflation even as the economy starts to slow.

With soaring asking prices, housing affordability in NYC continues to be a challenge. The additional rate hike could deal another blow to hopeful buyers by making it more expensive to obtain a mortgage. However, it’s important to note that mortgage rates will be driven by markets’ response to the Fed’s overall messaging on Wednesday, rather than the rate hike itself.

Higher Mortgage Rates Could Squeeze NYC Buyers

When mortgage rates increase, monthly principal and interest (P&I) payments increase accordingly, holding home sales prices constant. When a buyer applies for a mortgage, lenders consider the ratio of expected monthly P&I payments and other housing expenses to the buyer’s income to determine how much loan a buyer can comfortably afford. Lenders commonly impose a 28% maximum on this ratio depending on credit score, a widely accepted rule among lenders. Bound by this cap, when interest rates rise, a buyer must reduce the loan value by either increasing their down payment or looking for a less expensive home.

For example, the 30-year fixed mortgage rate averaged 5.54% during the week of July 21. The median asking price in NYC rose 4.8% year-over-year to $995K in Q2 2022, the highest reading since 2018. Based on StreetEasy’s Mortgage Calculator, the monthly P&I payment on a $995K home would be $4,540, assuming a 20% down payment. If the interest rate rises by one percentage point to 6.54%, that monthly payment would rise by $513 to $5,052. To keep the monthly payment at $4,540, a buyer would have to commit $100,957 more in down payment, a staggering amount that would take a household earning the median income in the NYC area about 15 months to earn. The impact can be larger when other expenses such as homeowners’ insurance and maintenance costs are taken into account.

Affordability Has Already Deteriorated Rapidly in All Boroughs

Using the same methodology, we estimate that a potential one percentage point increase in mortgage rates could cost Manhattan buyers at least $150K, based on the expected increases in monthly P&I payments on the median price home in the borough. In Brooklyn and Queens, it would cost buyers $100K and $65K, respectively.

In addition to the run-up in rates this year, median asking prices rose sharply in all boroughs, driven by a rebound in buyer demand. In Manhattan, the median asking price reached $1.5M in June (+10.7% year-over-year), the highest since June 2020. In Brooklyn, median asking price rose to $1M in June (+7.9% year-over-year), a new record high in StreetEasy data. In Queens, median asking price hit $644K in June (+7.4% year-over-year), the highest since September 2020.

As a result, monthly P&I payments picked up considerably. Based on StreetEasy’s historical data and the prevailing 30-year mortgage rate at the time, the monthly P&I payment for a median price home in Manhattan was at $5,045 in December 2021. By June, it had risen 38% to $6,942. In both Brooklyn and Queens, monthly payments rose by 51%: from $3,078 to $4,634 for Brooklyn, and $1,984 to $2,988 for Queens.

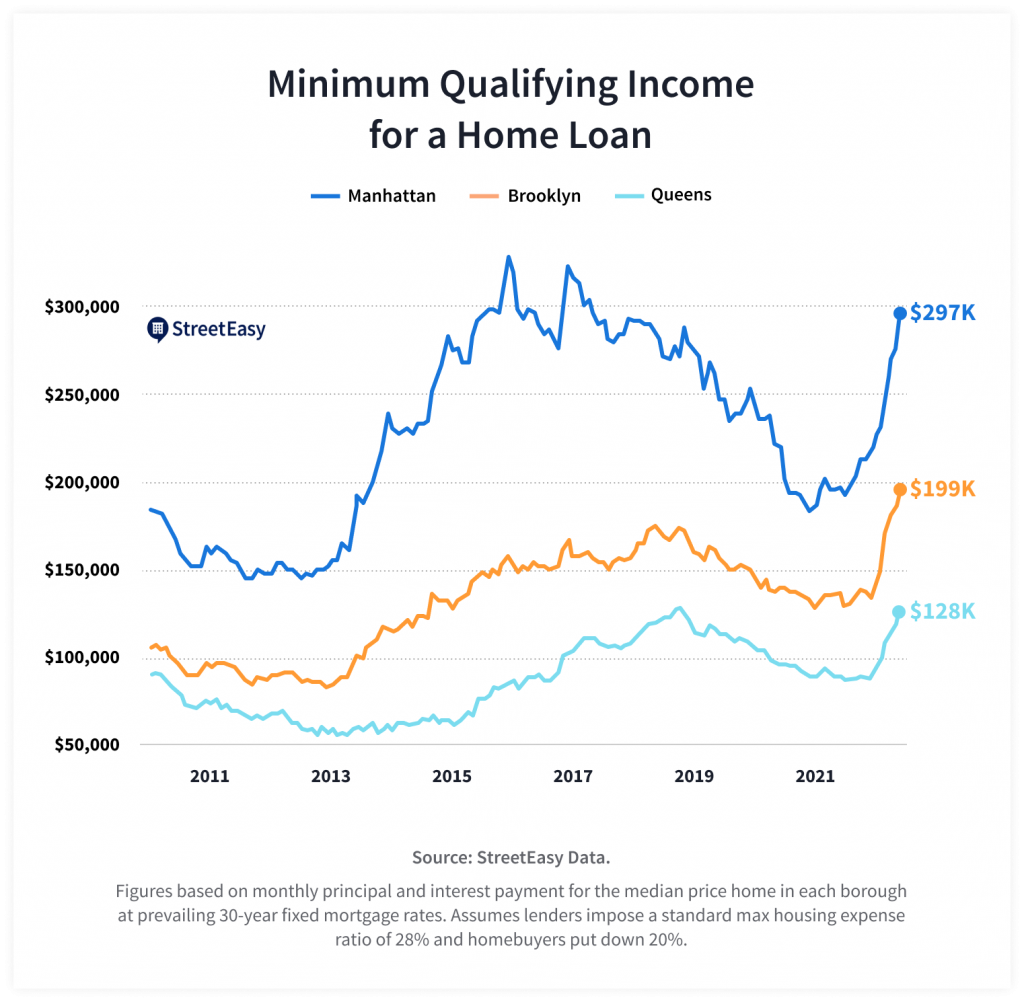

Even Prior to Rate Hikes, NYC Buyers Needed 50% More Income

Higher mortgage expenses warrant a higher minimum income necessary to qualify for a loan, making it more challenging for prospective buyers to afford a home in a competitive market. Minimum qualifying annual income to afford the median price home rose strongly in all three boroughs, assuming a 28% maximum housing expense to income ratio and 20% down payment. In Manhattan, minimum qualifying income rose 52% year-over-year to $297K in June. In Brooklyn, it reached $199K, up 48% year-over-year. In Queens, it increased 48% year-over-year to $128K.

June 2022’s qualifying income of almost $300K in Manhattan was the highest on StreetEasy record since 2017. This suggests only the top 5% of households in the NYC metro area can afford homeownership in Manhattan, based on the latest income distribution data. A decade ago the minimum qualifying income was $148K ($193K in today’s dollars), putting homeownership within reach for nearly 20% of Manhattan households.

Homebuyer Demand Has Passed the Inflection Point

After strong sales activity in 2021, signs of slowing buyer demand are emerging as affordability continues to worsen. More homes went into contract in Q2 in Manhattan, Brooklyn, and Queens than in Q1 this year, but were down compared to strong sales activity last year. The number of NYC homes going into contract started to decline on a monthly basis starting in April through mid-July, even after adjusting for a seasonal slowdown around the summer holidays. Due to cumulative interest rate increases, sales activity will continue to moderate this year.

Despite early signs of softening demand, we are still in a seller’s market. The median days on market for an NYC home fell to 49 days in Q2 from 78 days in Q1. The current level remains well below the pre-pandemic average as demand continues to outpace available homes for sale. Sales inventory in NYC continued to fall in Q2 2022, down 6% from Q2 2021. Moreover, higher interest rates can temporarily slow inventory growth. Homeowners wishing to sell their primary residence may be reluctant to do so, as they’d have to abandon the lower interest rate they’re already locked into – the so-called “rate lock-in” effect. This is negative for inventory, and makes the market that much more competitive for buyers.

Interest Rate Outlook Remains Uncertain

As previously mentioned, the Fed’s rate hike on Wednesday will not directly result in a rise in mortgage rates by the same amount. The rates on 30-year mortgages that many households use to finance their home are inextricably linked to yields on 10-year US Treasury notes, often determined by financial market forces. To some extent, current mortgage rates already reflect the rate hike announcement on Wednesday. What’s less certain is how aggressive the Fed’s future rate hikes will be, and the severity of the resulting economic slowdown in 2023—which will drive market pricing for 10-year US Treasury notes and consequently 30-year mortgage rates.

Ultimately, upcoming inflation data will influence market predictions for the Fed’s monetary policy over the coming weeks. After the Fed showed its willingness to raise interest rates expeditiously to fight inflation earlier this year, market pricing for government debts changed rapidly, leading to 30-year fixed mortgage rates soaring to 5.5% as of last week from 3.1% on average in December. With inflationary forces spreading to a broader range of goods and services, stronger inflation data over the next few weeks has the potential to force the Fed to signal even more aggressive rate hikes. If markets react strongly, a one percentage point increase in long-term interest rates is a possibility.

However, the prospect of slower economic growth in 2023 looms over financial markets, weighing on yields on Treasury notes. The decline in mortgage rates last week was related to financial markets’ assessment of recession risk in 2023. Interest rates will remain volatile due to the prospect of slowing US economic growth and persistently high inflation.